Presentation Summary

Explore the future of cinema with a focus on market stabilization, regional dynamics, and industry transformation in the 2025-2026 period.

Full Presentation Transcript

Slide 1: The Global Cinema Renaissance: Navigating Movies, Markets & Momentum in 2025-2026

A comprehensive exploration of the evolving theatrical and streaming landscape across global markets, regional dynamics, and industry transformation.

Slide 2: Contents

- Market Foundation: Industry stabilization and theatrical landscape.

- Regional Markets: Singapore and Johor Bahru cinema ecosystems.

- Content & Curation: Current releases and 2025-2026 films.

- Industry Transformation: Streaming models and technology integration.

- Strategic Outlook: Global dynamics and economic projections through 2029.

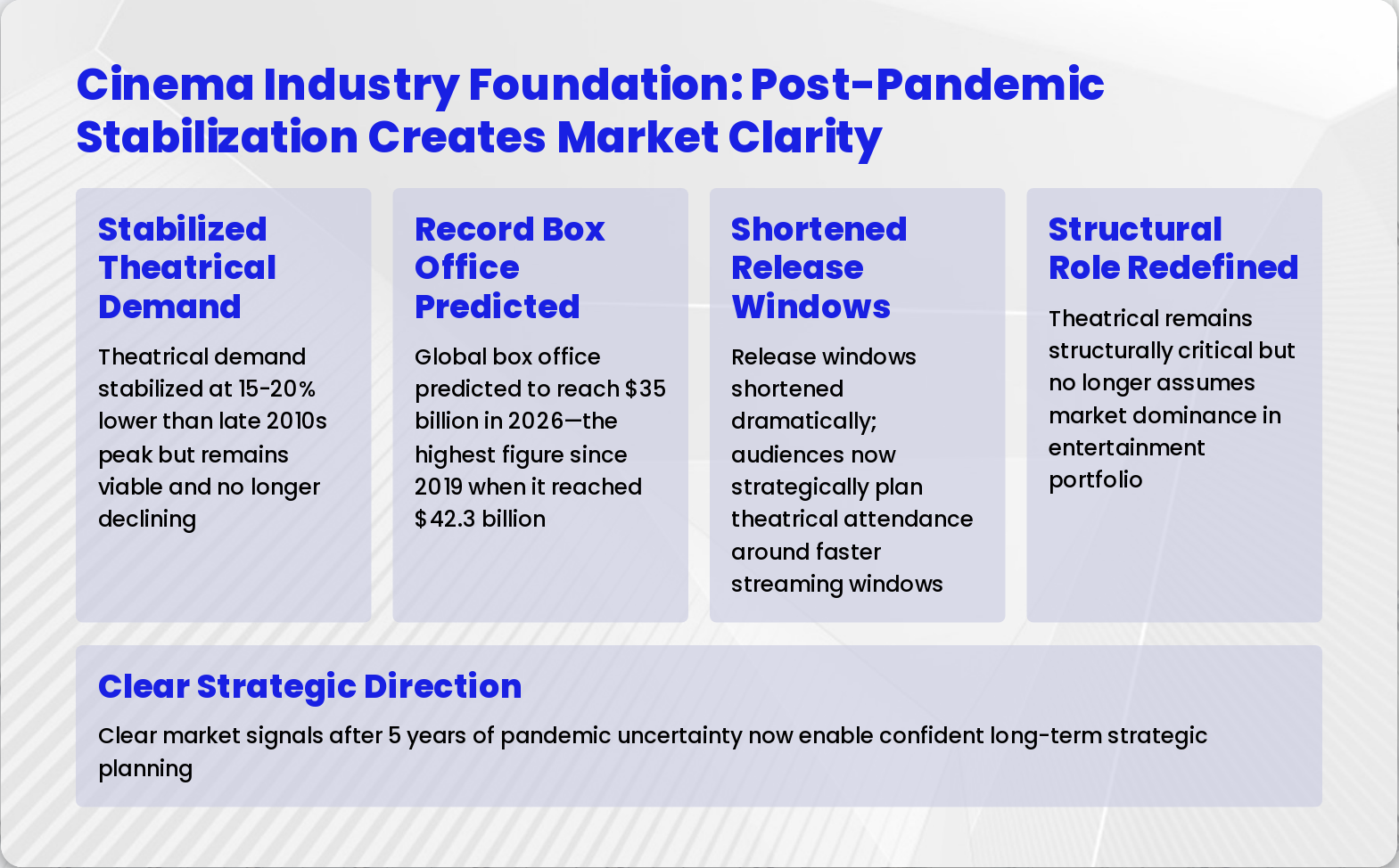

Slide 3: Cinema Industry Foundation: Post-Pandemic Stabilization Creates Market Clarity

- Stabilized Theatrical Demand: Theatrical demand stabilized at 15-20% lower than late 2010s peak but remains viable and no longer declining

- Record Box Office Predicted: Global box office predicted to reach $35 billion in 2026—the highest figure since 2019 when it reached $42.3 billion

- Shortened Release Windows: Release windows shortened dramatically; audiences now strategically plan theatrical attendance around faster streaming windows

- Structural Role Redefined: Theatrical remains structurally critical but no longer assumes market dominance in entertainment portfolio

- Clear Strategic Direction: Clear market signals after 5 years of pandemic uncertainty now enable confident long-term strategic planning

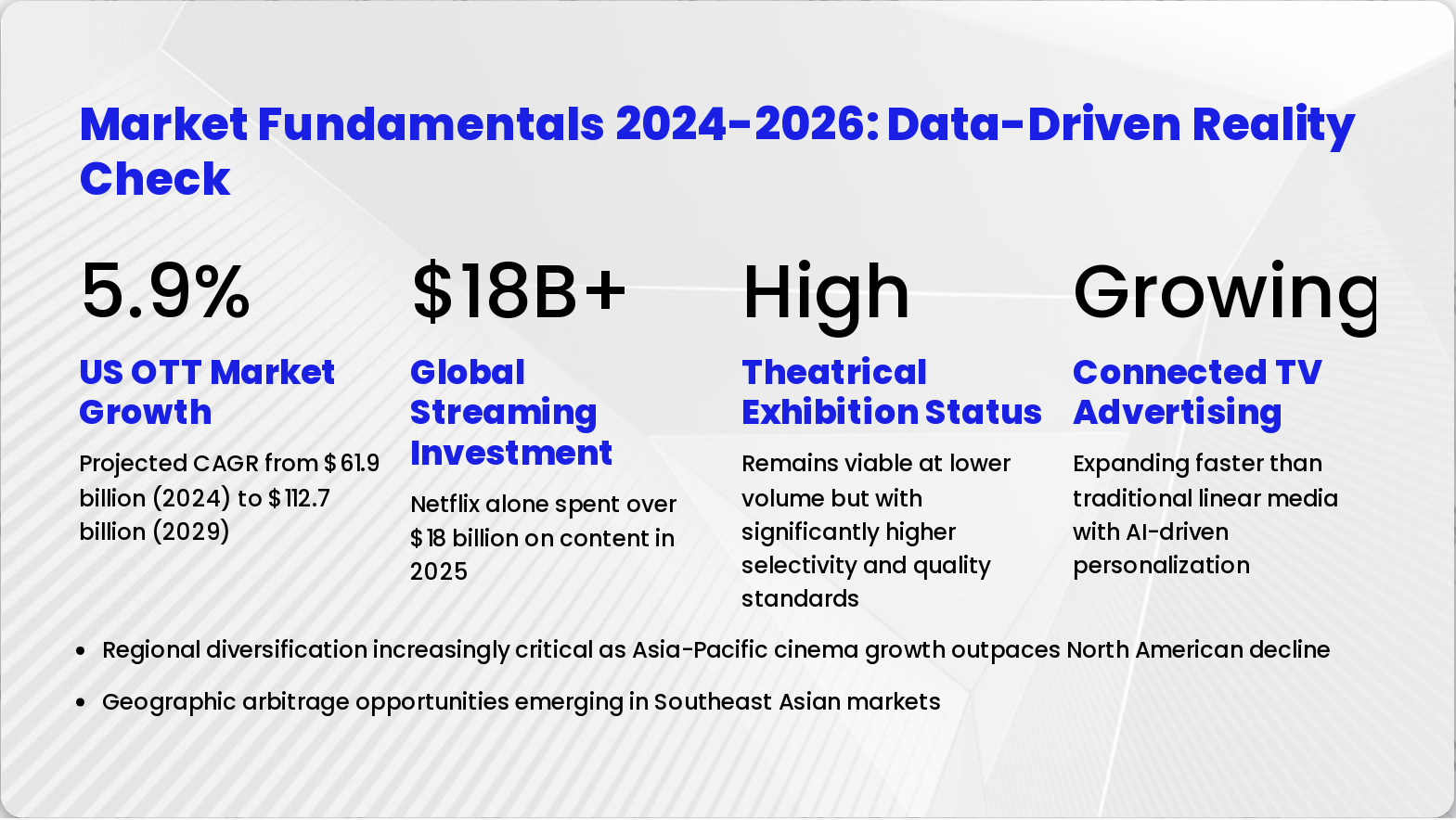

Slide 4: Market Fundamentals 2024-2026: Data-Driven Reality Check

- 5.9% — US OTT Market Growth

- $18B+ — Global Streaming Investment

- High — Theatrical Exhibition Status

- Growing — Connected TV Advertising

Regional diversification increasingly critical as Asia-Pacific cinema growth outpaces North American decline

Geographic arbitrage opportunities emerging in Southeast Asian markets

- Regional diversification increasingly critical as Asia-Pacific cinema growth outpaces North American decline

- Geographic arbitrage opportunities emerging in Southeast Asian markets

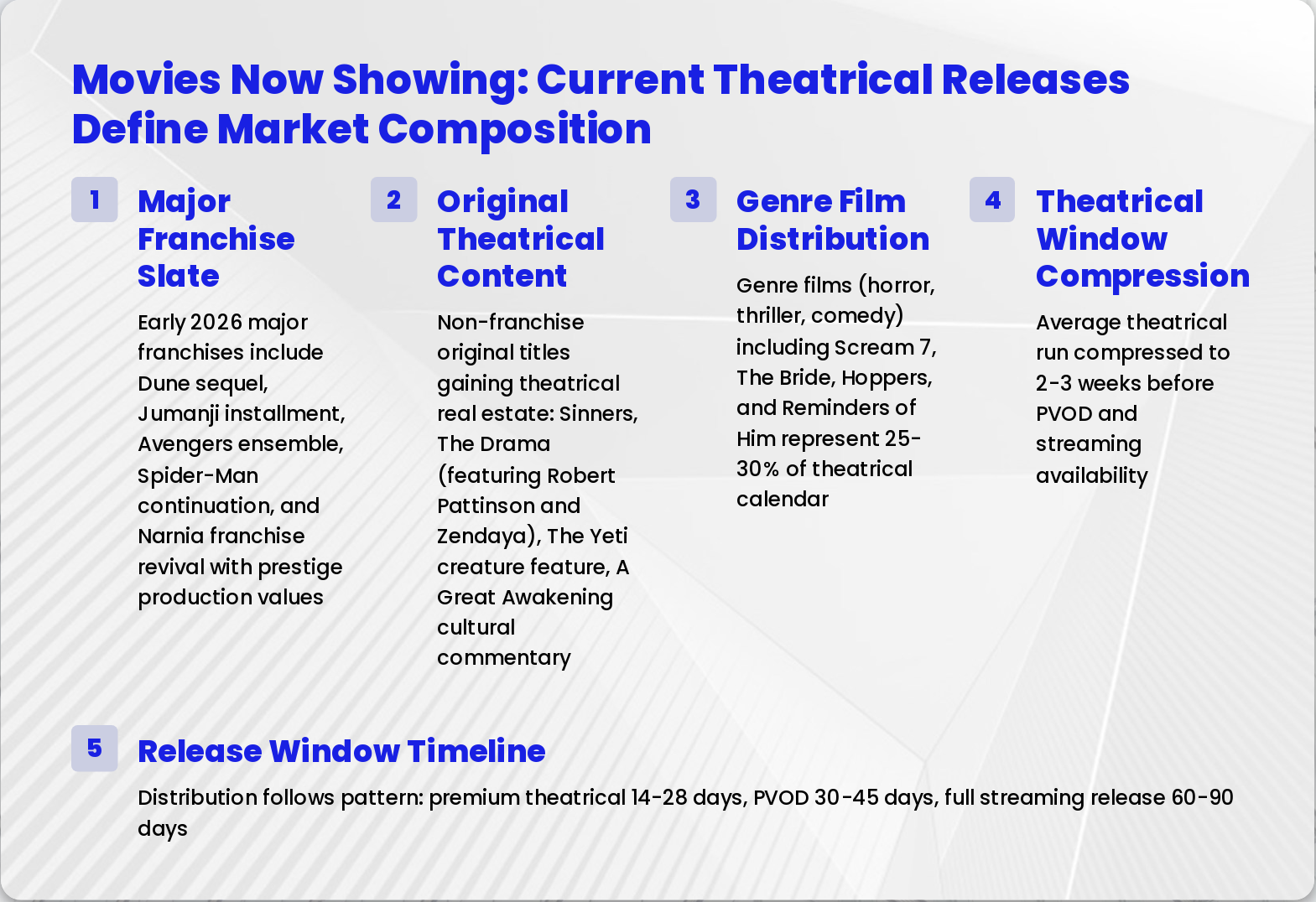

Slide 5: Movies Now Showing: Current Theatrical Releases Define Market Composition

- Major Franchise Slate: Early 2026 major franchises include Dune sequel, Jumanji installment, Avengers ensemble, Spider-Man continuation, and Narnia franchise revival with prestige production values

- Original Theatrical Content: Non-franchise original titles gaining theatrical real estate: Sinners, The Drama (featuring Robert Pattinson and Zendaya), The Yeti creature feature, A Great Awakening cultural commentary

- Genre Film Distribution: Genre films (horror, thriller, comedy) including Scream 7, The Bride, Hoppers, and Reminders of Him represent 25-30% of theatrical calendar

- Theatrical Window Compression: Average theatrical run compressed to 2-3 weeks before PVOD and streaming availability

- Release Window Timeline: Distribution follows pattern: premium theatrical 14-28 days, PVOD 30-45 days, full streaming release 60-90 days

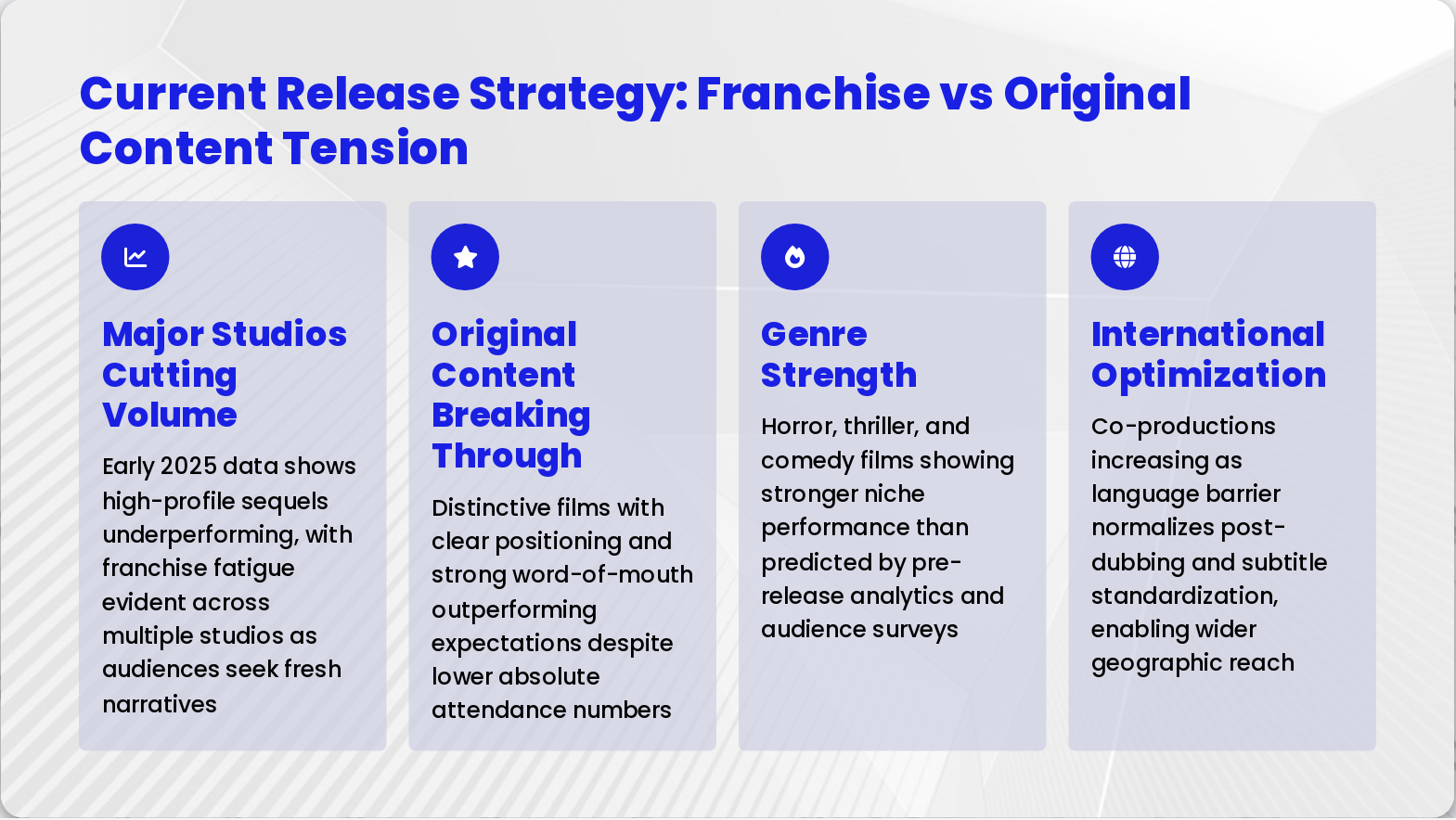

Slide 6: Current Release Strategy: Franchise vs Original Content Tension

- Major Studios Cutting Volume: Early 2025 data shows high-profile sequels underperforming, with franchise fatigue evident across multiple studios as audiences seek fresh narratives

- Original Content Breaking Through: Distinctive films with clear positioning and strong word-of-mouth outperforming expectations despite lower absolute attendance numbers

- Genre Strength: Horror, thriller, and comedy films showing stronger niche performance than predicted by pre-release analytics and audience surveys

- International Optimization: Co-productions increasing as language barrier normalizes post-dubbing and subtitle standardization, enabling wider geographic reach

Slide 7: Singapore Cinema Market: Strategic Geography & Premium Positioning

- Market Scale & Growth: Singapore cinema market valued at multiple millions USD in 2024 with forecasted CAGR growth2024-2033aligned with regional affluence and English-language content preference

- Market Leaders: Major cinema operators commanding80%+ market share: Golden Village and Shaw Theatres establish premium experience standards across the region

- Premium Technology: Premium large-format screens including IMAX and Dolby Cinema concentrated in Singapore, driving higher per-ticket revenue and audience attraction

- Affluent Demographics: Audience demographics skew affluent, educated, and multilingual with strategic position as Southeast Asian media hub influencing content acquisition and release timing

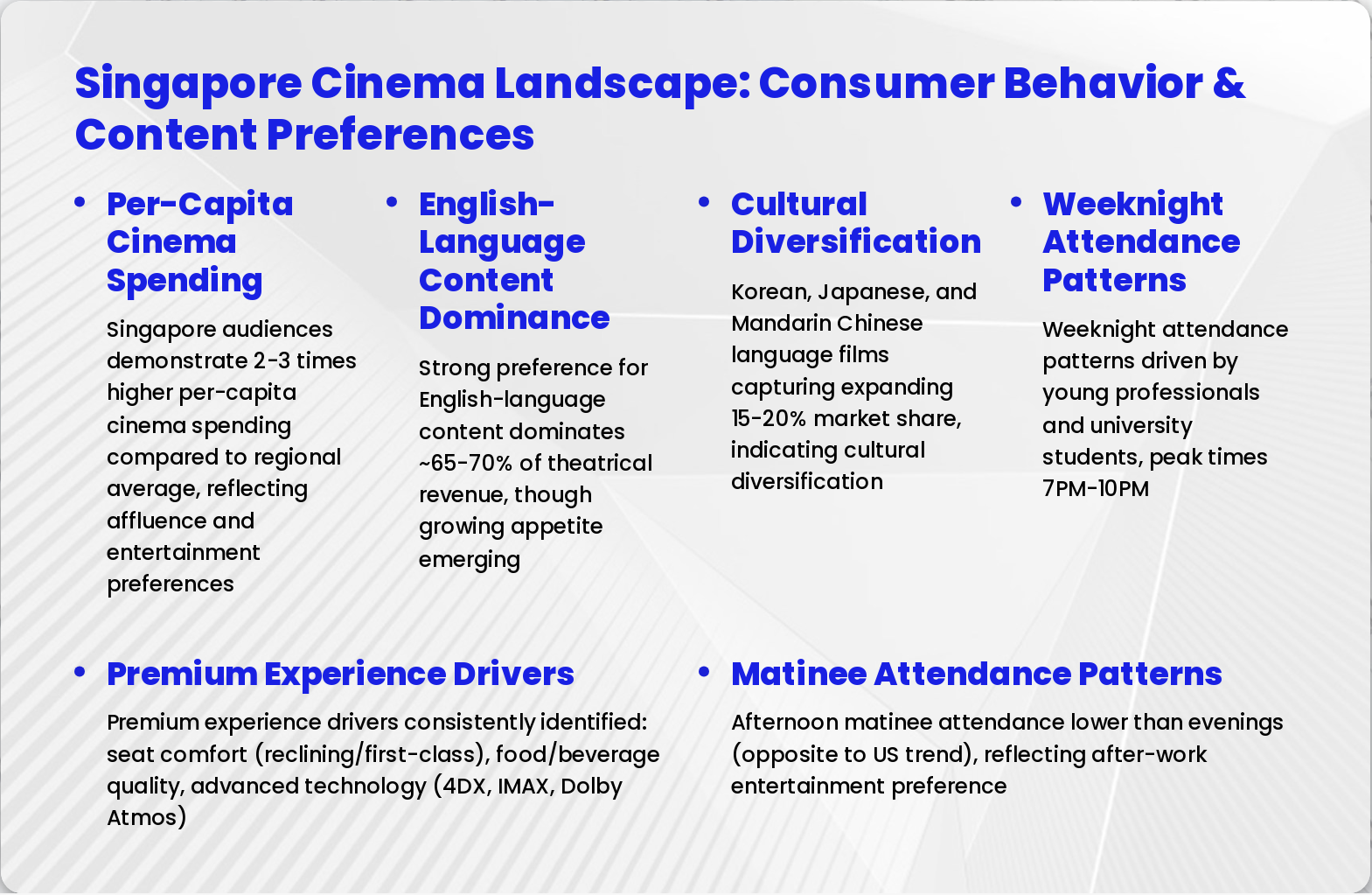

Slide 8: Singapore Cinema Landscape: Consumer Behavior & Content Preferences

- Per-Capita Cinema Spending: Singapore audiences demonstrate 2-3 times higher per-capita cinema spending compared to regional average, reflecting affluence and entertainment preferences

- English-Language Content Dominance: Strong preference for English-language content dominates ~65-70% of theatrical revenue, though growing appetite emerging

- Cultural Diversification: Korean, Japanese, and Mandarin Chinese language films capturing expanding 15-20% market share, indicating cultural diversification

- Weeknight Attendance Patterns: Weeknight attendance patterns driven by young professionals and university students, peak times 7PM-10PM

- Premium Experience Drivers: Premium experience drivers consistently identified: seat comfort (reclining/first-class), food/beverage quality, advanced technology (4DX, IMAX, Dolby Atmos)

- Matinee Attendance Patterns: Afternoon matinee attendance lower than evenings (opposite to US trend), reflecting after-work entertainment preference

Slide 9: Johor Bahru Cinema Market: Cross-Border Dynamics & Value Proposition

- Cross-Border Destination Appeal: Johor Bahru positioned as cross-border cinema destination attracting Malaysian and Singapore audiences with equivalent release parity and competitive entertainment options.

- Cinema Hopping Culture: Singapore residents strategically cross-border seeking30-40% better value withRM-SGD currency advantage, creating significant demand momentum.

- Competitive Operator Footprint: Major operators TGV and GSC establishing competitive footprint, investing in premium formats to compete upmarket and capture cross-border audiences.

- Ticket Price Economics: RM12-18 per ticket versus SGD12-16+ in Singapore creates margin arbitrage driving cross-border attendance and customer acquisition patterns.

- Growing Middle-Class Consumer Base: Expanding Malaysian middle-class consumer base driving attendance growth with lifestyle entertainment spending acceleration and rising disposable income.

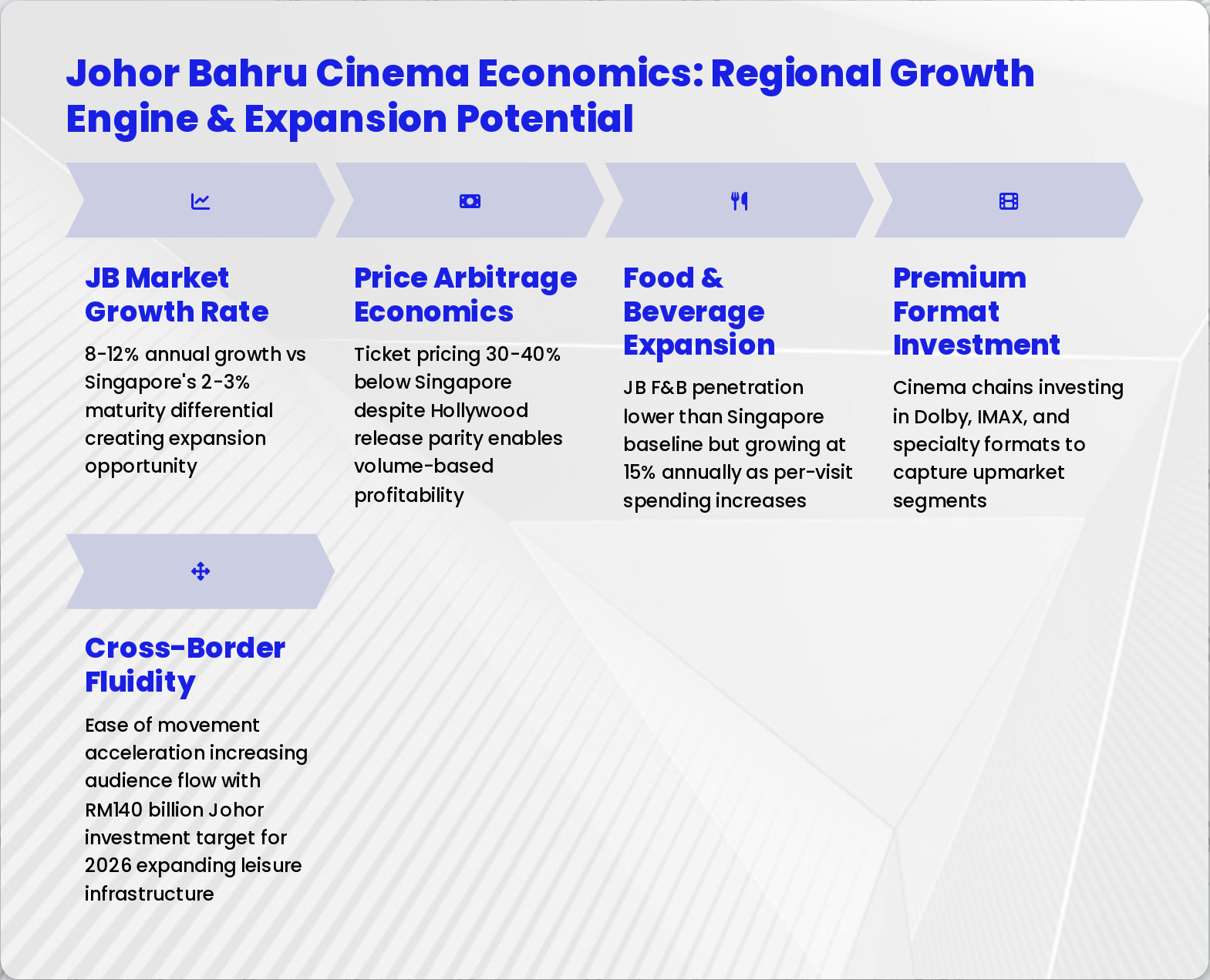

Slide 10: Johor Bahru Cinema Economics: Regional Growth Engine & Expansion Potential

- JB Market Growth Rate: 8-12% annual growth vs Singapore's 2-3% maturity differential creating expansion opportunity

- Price Arbitrage Economics: Ticket pricing 30-40% below Singapore despite Hollywood release parity enables volume-based profitability

- Food & Beverage Expansion: JB F&B penetration lower than Singapore baseline but growing at 15% annually as per-visit spending increases

- Premium Format Investment: Cinema chains investing in Dolby, IMAX, and specialty formats to capture upmarket segments

- Cross-Border Fluidity: Ease of movement acceleration increasing audience flow with RM140 billion Johor investment target for 2026 expanding leisure infrastructure

Slide 11: Movies to Watch: Strategic Selection Framework for 2025-2026

- Audience Positioning: Clear promise to specific demographic rather than mass-appeal approach, enabling targeted word-of-mouth and community building

- Production Quality: Technical excellence no longer dependent on budget; AI tools and democratized software enable high visual fidelity at lower cost

- Narrative Authenticity: Original stories with fresh storytelling approach outperform derivative content; audiences signal reward for creative distinctiveness

- Cultural Relevance: Thematic resonance with contemporary audience concerns including social issues, identity, and future orientation

- Platform Strategy: Evaluate theatrical worthiness vs formats optimized for streaming consumption; consider audience device preferences

- Regional Availability: Account for English-language releases, dubbed versions, and subtitled options available across Singapore and Johor Bahru cinema networks

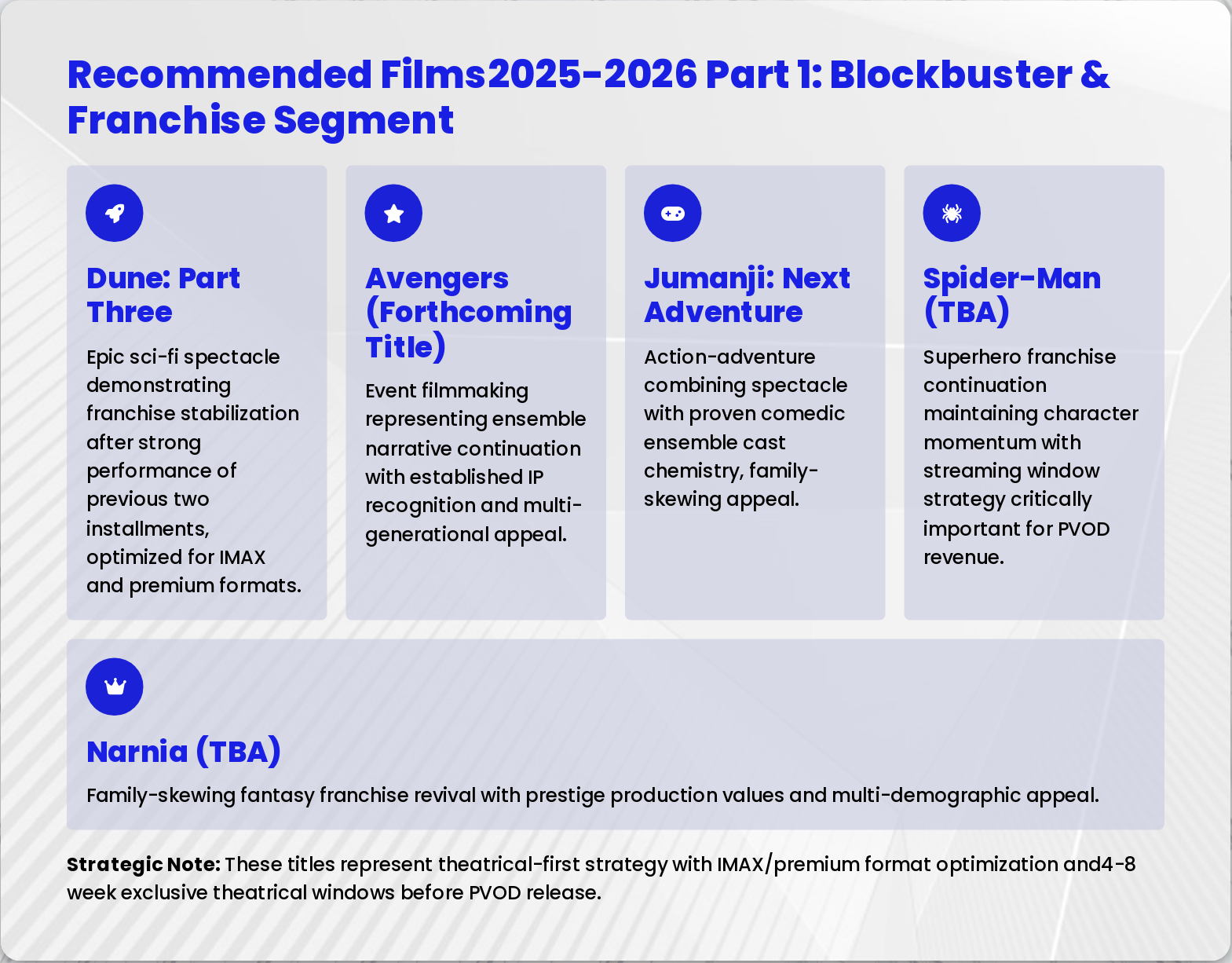

Slide 12: Recommended Films2025-2026 Part 1: Blockbuster & Franchise Segment

- Dune: Part Three: Epic sci-fi spectacle demonstrating franchise stabilization after strong performance of previous two installments, optimized for IMAX and premium formats.

- Avengers (Forthcoming Title): Event filmmaking representing ensemble narrative continuation with established IP recognition and multi-generational appeal.

- Jumanji: Next Adventure: Action-adventure combining spectacle with proven comedic ensemble cast chemistry, family-skewing appeal.

- Spider-Man (TBA): Superhero franchise continuation maintaining character momentum with streaming window strategy critically important for PVOD revenue.

- Narnia (TBA): Family-skewing fantasy franchise revival with prestige production values and multi-demographic appeal.

Strategic Note: These titles represent theatrical-first strategy with IMAX/premium format optimization and4-8 week exclusive theatrical windows before PVOD release.

Slide 13: Recommended Films 2025-2026 Part 2: Original & Genre-Driven Selection

- Sinners (2025): Original drama with distinctive audience positioning and demonstrated word-of-mouth driver appeal; breaks through marketplace noise with authentic narrative voice

- The Drama (April 2026): Original project featuring Robert Pattinson and Zendaya representing prestige casting in non-franchise context; strong awards-season positioning

- The Yeti (2026): Genre creature-feature film leveraging creature-design appeal; niche audience targeting with potential franchise positioning if successful

- A Great Awakening (2026): Original narrative feature with cultural commentary and social relevance, positioning for international festival and prestige distribution

- Korean and Japanese Releases: Growing theatrical availability of subtitled and dubbed versions across Singapore and Johor Bahru cinema networks; expanding non-English content market share

- Platform Strategy Recommendation: Theatrical release for major franchises (Dune, Avengers, Spider-Man); streaming-first for mid-budget originals; selective theatrical release for high-concept genre films based on audience research

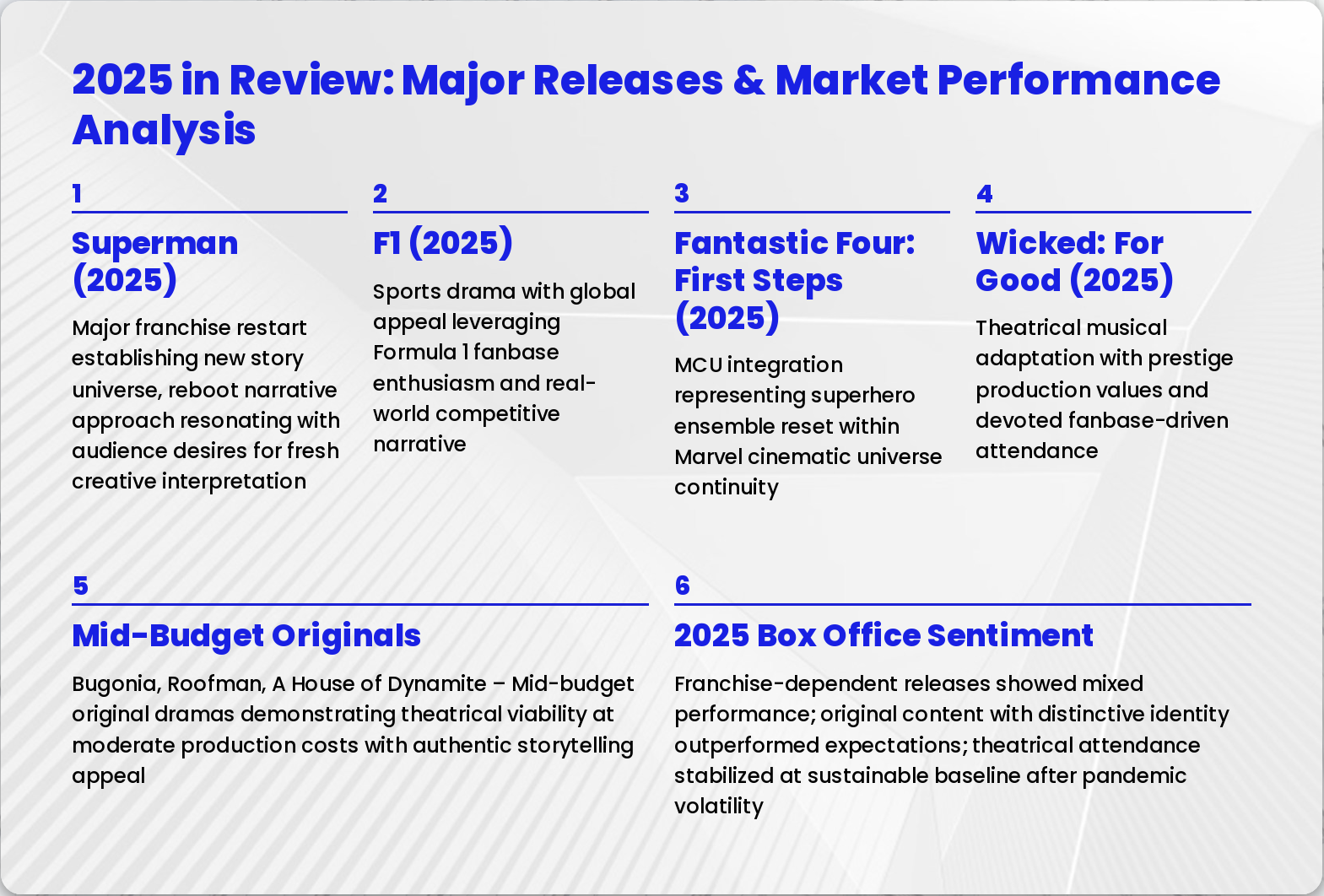

Slide 14: 2025 in Review: Major Releases & Market Performance Analysis

- Superman (2025): Major franchise restart establishing new story universe, reboot narrative approach resonating with audience desires for fresh creative interpretation

- F1 (2025): Sports drama with global appeal leveraging Formula 1 fanbase enthusiasm and real-world competitive narrative

- Fantastic Four: First Steps (2025): MCU integration representing superhero ensemble reset within Marvel cinematic universe continuity

- Wicked: For Good (2025): Theatrical musical adaptation with prestige production values and devoted fanbase-driven attendance

- Mid-Budget Originals: Bugonia, Roofman, A House of Dynamite – Mid-budget original dramas demonstrating theatrical viability at moderate production costs with authentic storytelling appeal

- 2025 Box Office Sentiment: Franchise-dependent releases showed mixed performance; original content with distinctive identity outperformed expectations; theatrical attendance stabilized at sustainable baseline after pandemic volatility

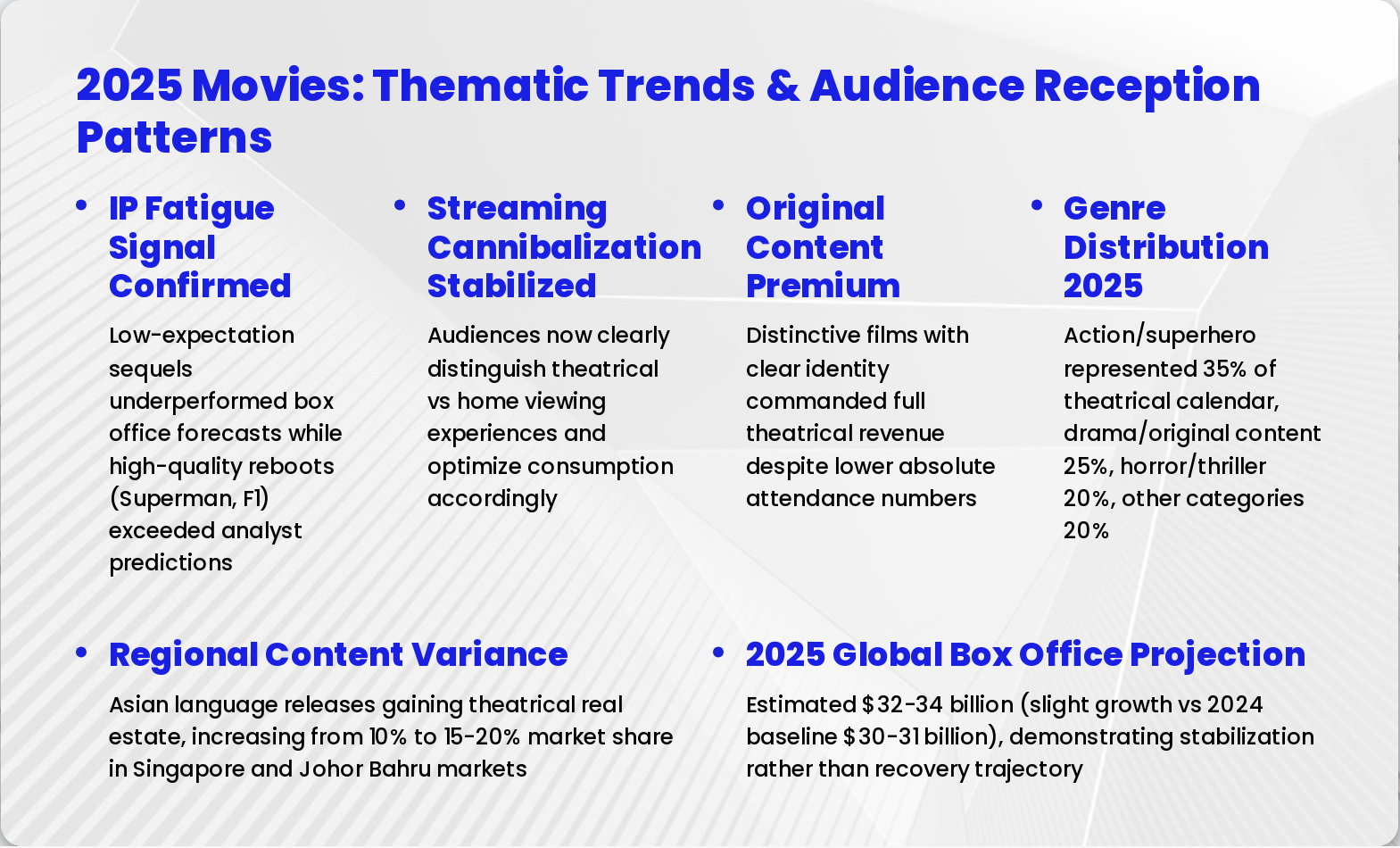

Slide 15: 2025 Movies: Thematic Trends & Audience Reception Patterns

- IP Fatigue Signal Confirmed: Low-expectation sequels underperformed box office forecasts while high-quality reboots (Superman, F1) exceeded analyst predictions

- Streaming Cannibalization Stabilized: Audiences now clearly distinguish theatrical vs home viewing experiences and optimize consumption accordingly

- Original Content Premium: Distinctive films with clear identity commanded full theatrical revenue despite lower absolute attendance numbers

- Genre Distribution 2025: Action/superhero represented 35% of theatrical calendar, drama/original content 25%, horror/thriller 20%, other categories 20%

- Regional Content Variance: Asian language releases gaining theatrical real estate, increasing from 10% to 15-20% market share in Singapore and Johor Bahru markets

- 2025 Global Box Office Projection: Estimated $32-34 billion (slight growth vs 2024 baseline $30-31 billion), demonstrating stabilization rather than recovery trajectory

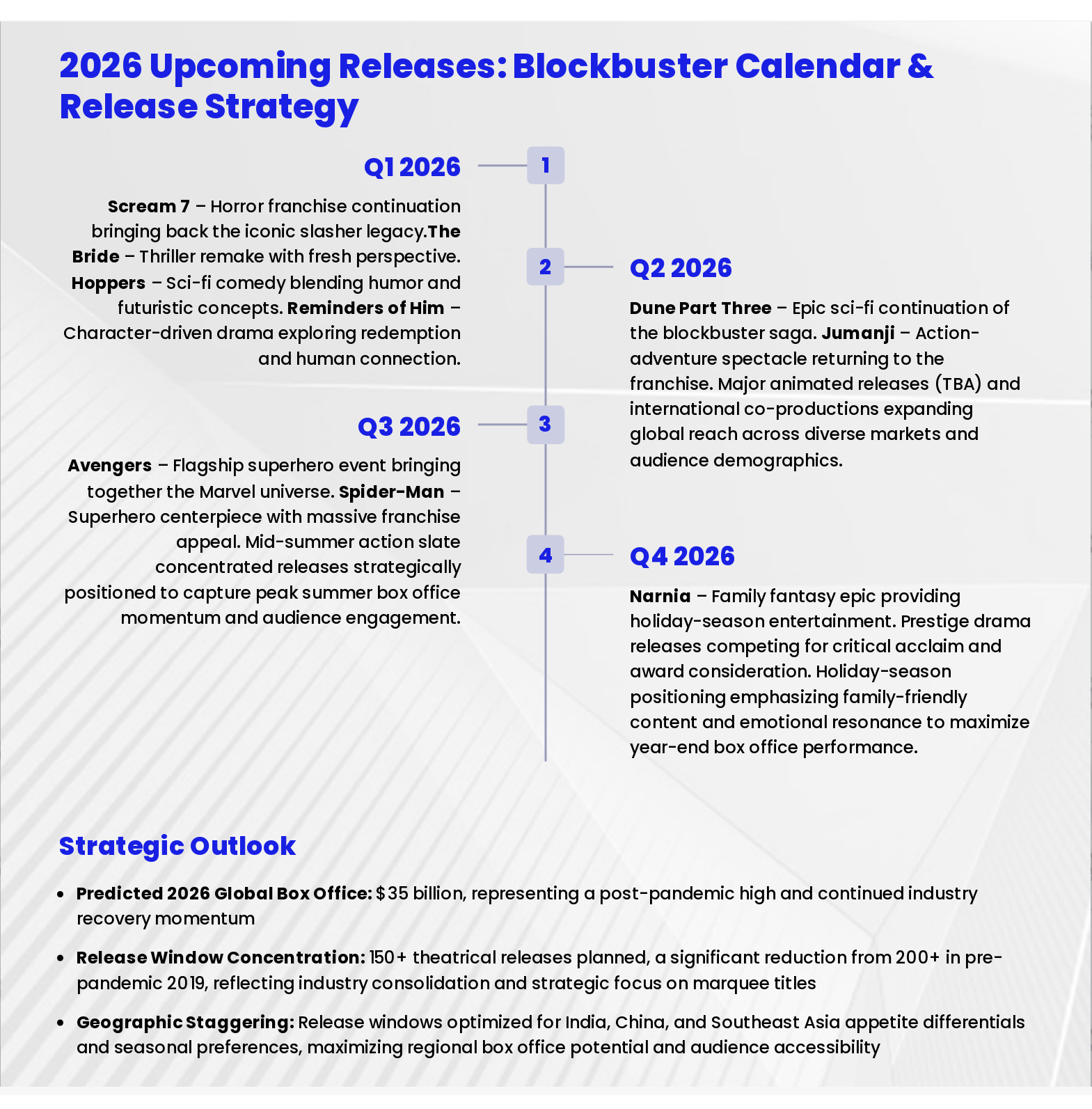

Slide 16: 2026 Upcoming Releases: Blockbuster Calendar & Release Strategy

- Q1 2026: Scream 7 – Horror franchise continuation bringing back the iconic slasher legacy. The Bride – Thriller remake with fresh perspective. Hoppers – Sci-fi comedy blending humor and futuristic concepts. Reminders of Him – Character-driven drama exploring redemption and human connection.

- Q2 2026: Dune Part Three – Epic sci-fi continuation of the blockbuster saga. Jumanji – Action-adventure spectacle returning to the franchise. Major animated releases (TBA) and international co-productions expanding global reach across diverse markets and audience demographics.

- Q3 2026: Avengers – Flagship superhero event bringing together the Marvel universe. Spider-Man – Superhero centerpiece with massive franchise appeal. Mid-summer action slate concentrated releases strategically positioned to capture peak summer box office momentum and audience engagement.

- Q4 2026: Narnia – Family fantasy epic providing holiday-season entertainment. Prestige drama releases competing for critical acclaim and award consideration. Holiday-season positioning emphasizing family-friendly content and emotional resonance to maximize year-end box office performance.

Predicted 2026 Global Box Office: $35 billion, representing a post-pandemic high and continued industry recovery momentum

Release Window Concentration: 150+ theatrical releases planned, a significant reduction from 200+ in pre-pandemic 2019, reflecting industry consolidation and strategic focus on marquee titles

Geographic Staggering: Release windows optimized for India, China, and Southeast Asia appetite differentials and seasonal preferences, maximizing regional box office potential and audience accessibility

- Predicted 2026 Global Box Office: $35 billion, representing a post-pandemic high and continued industry recovery momentum

- Release Window Concentration: 150+ theatrical releases planned, a significant reduction from 200+ in pre-pandemic 2019, reflecting industry consolidation and strategic focus on marquee titles

- Geographic Staggering: Release windows optimized for India, China, and Southeast Asia appetite differentials and seasonal preferences, maximizing regional box office potential and audience accessibility

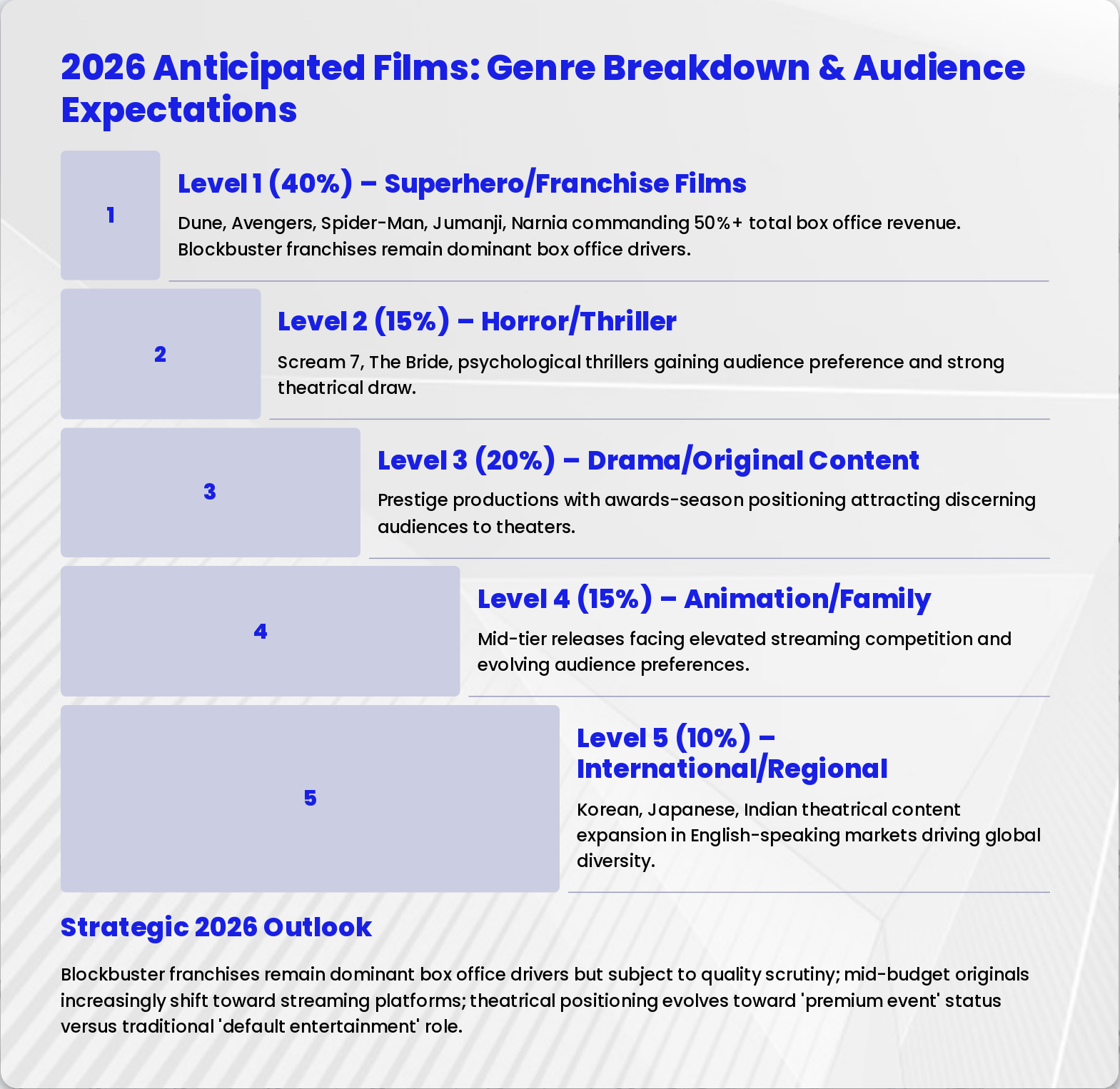

Slide 17: 2026 Anticipated Films: Genre Breakdown & Audience Expectations

- Level 1 (40%) – Superhero/Franchise Films: Dune, Avengers, Spider-Man, Jumanji, Narnia commanding 50%+ total box office revenue. Blockbuster franchises remain dominant box office drivers.

- Level 2 (15%) – Horror/Thriller: Scream 7, The Bride, psychological thrillers gaining audience preference and strong theatrical draw.

- Level 3 (20%) – Drama/Original Content: Prestige productions with awards-season positioning attracting discerning audiences to theaters.

- Level 4 (15%) – Animation/Family: Mid-tier releases facing elevated streaming competition and evolving audience preferences.

- Level 5 (10%) – International/Regional: Korean, Japanese, Indian theatrical content expansion in English-speaking markets driving global diversity.

Blockbuster franchises remain dominant box office drivers but subject to quality scrutiny; mid-budget originals increasingly shift toward streaming platforms; theatrical positioning evolves toward 'premium event' status versus traditional 'default entertainment' role.

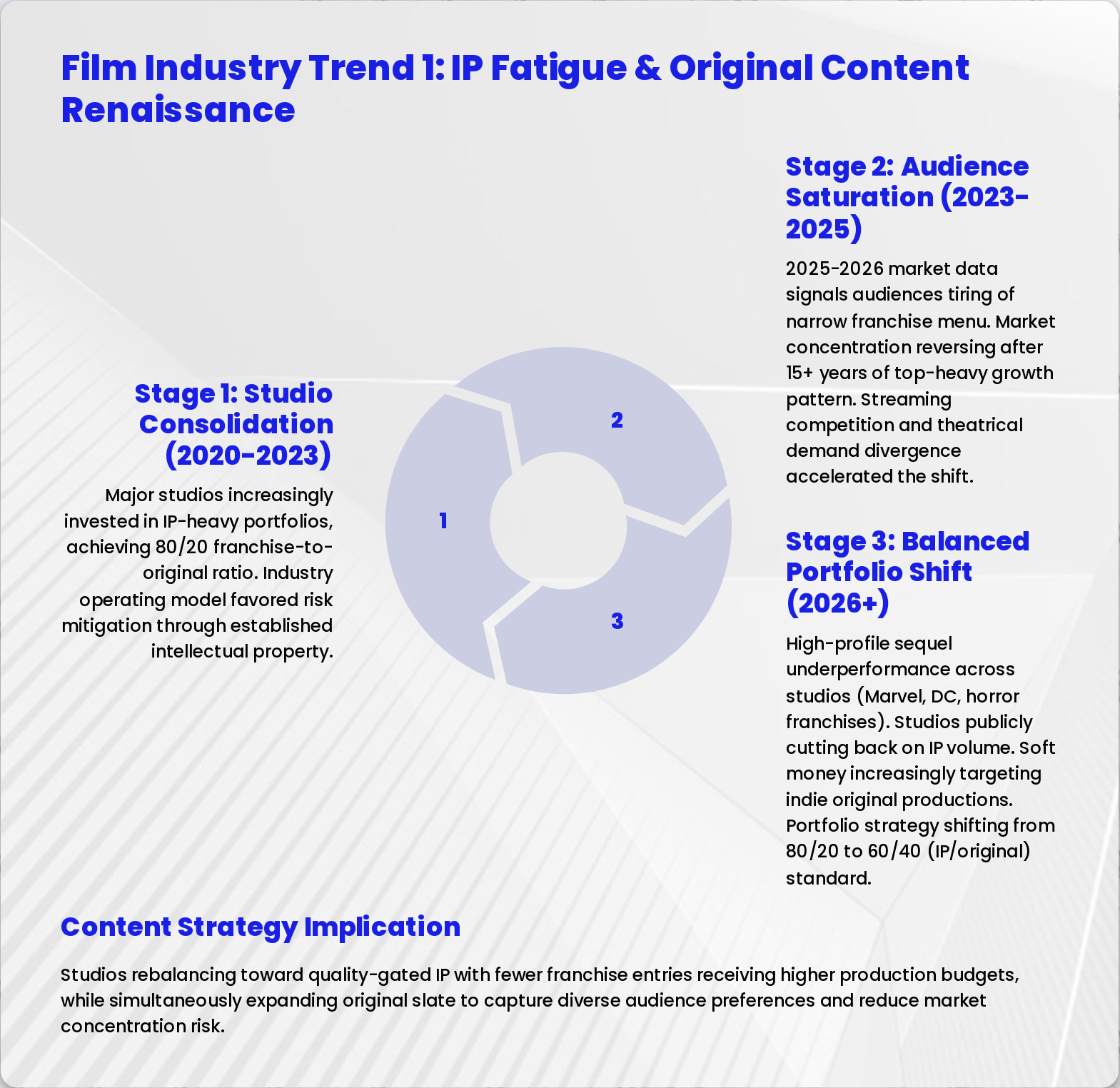

Slide 18: Film Industry Trend 1: IP Fatigue & Original Content Renaissance

- Stage 1: Studio Consolidation (2020-2023): Major studios increasingly invested in IP-heavy portfolios, achieving 80/20 franchise-to-original ratio. Industry operating model favored risk mitigation through established intellectual property.

- Stage 2: Audience Saturation (2023-2025): 2025-2026 market data signals audiences tiring of narrow franchise menu. Market concentration reversing after 15+ years of top-heavy growth pattern. Streaming competition and theatrical demand divergence accelerated the shift.

- Stage 3: Balanced Portfolio Shift (2026+): High-profile sequel underperformance across studios (Marvel, DC, horror franchises). Studios publicly cutting back on IP volume. Soft money increasingly targeting indie original productions. Portfolio strategy shifting from 80/20 to 60/40 (IP/original) standard.

Studios rebalancing toward quality-gated IP with fewer franchise entries receiving higher production budgets, while simultaneously expanding original slate to capture diverse audience preferences and reduce market concentration risk.

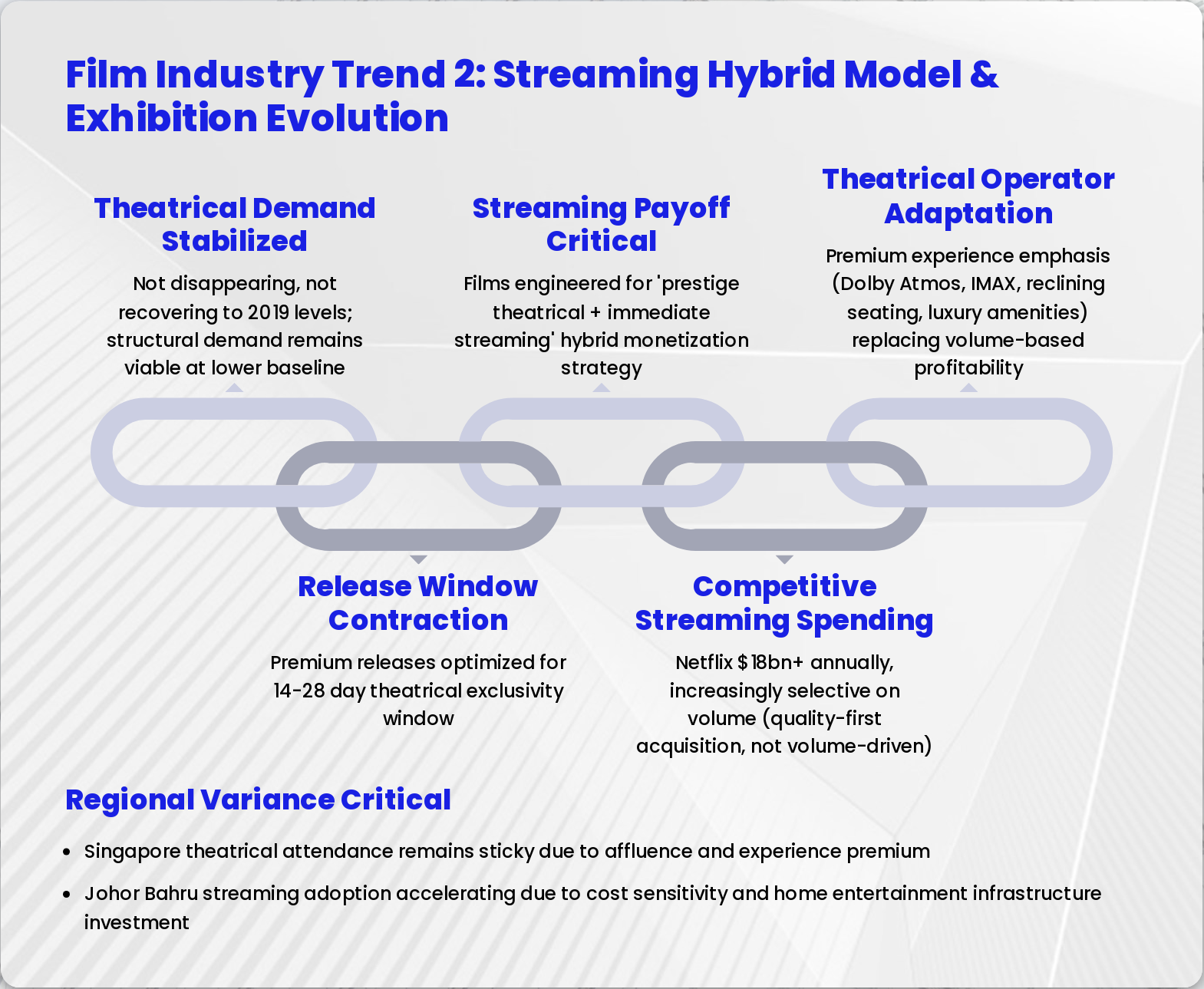

Slide 19: Film Industry Trend 2: Streaming Hybrid Model & Exhibition Evolution

- Theatrical Demand Stabilized: Not disappearing, not recovering to 2019 levels; structural demand remains viable at lower baseline

- Release Window Contraction: Premium releases optimized for 14-28 day theatrical exclusivity window

- Streaming Payoff Critical: Films engineered for 'prestige theatrical + immediate streaming' hybrid monetization strategy

- Competitive Streaming Spending: Netflix $18bn+ annually, increasingly selective on volume (quality-first acquisition, not volume-driven)

- Theatrical Operator Adaptation: Premium experience emphasis (Dolby Atmos, IMAX, reclining seating, luxury amenities) replacing volume-based profitability

Singapore theatrical attendance remains sticky due to affluence and experience premium

Johor Bahru streaming adoption accelerating due to cost sensitivity and home entertainment infrastructure investment

- Singapore theatrical attendance remains sticky due to affluence and experience premium

- Johor Bahru streaming adoption accelerating due to cost sensitivity and home entertainment infrastructure investment

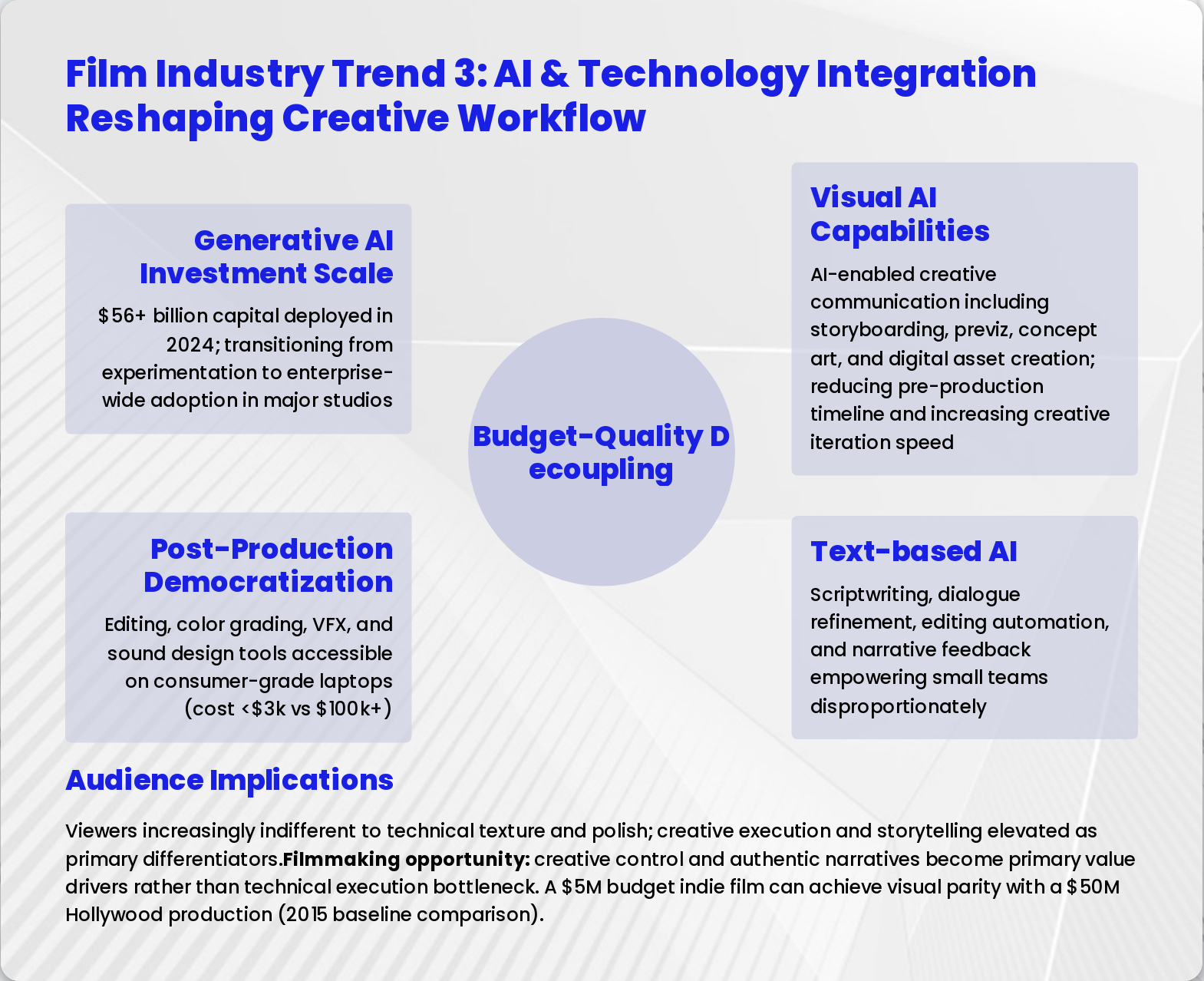

Slide 20: Film Industry Trend 3: AI & Technology Integration Reshaping Creative Workflow

- Generative AI Investment Scale: $56+ billion capital deployed in 2024; transitioning from experimentation to enterprise-wide adoption in major studios

- Visual AI Capabilities: AI-enabled creative communication including storyboarding, previz, concept art, and digital asset creation; reducing pre-production timeline and increasing creative iteration speed

- Text-based AI: Scriptwriting, dialogue refinement, editing automation, and narrative feedback empowering small teams disproportionately

- Post-Production Democratization: Editing, color grading, VFX, and sound design tools accessible on consumer-grade laptops (cost <$3k vs $100k+)

Viewers increasingly indifferent to technical texture and polish; creative execution and storytelling elevated as primary differentiators. Filmmaking opportunity: creative control and authentic narratives become primary value drivers rather than technical execution bottleneck. A $5M budget indie film can achieve visual parity with a $50M Hollywood production (2015 baseline comparison).

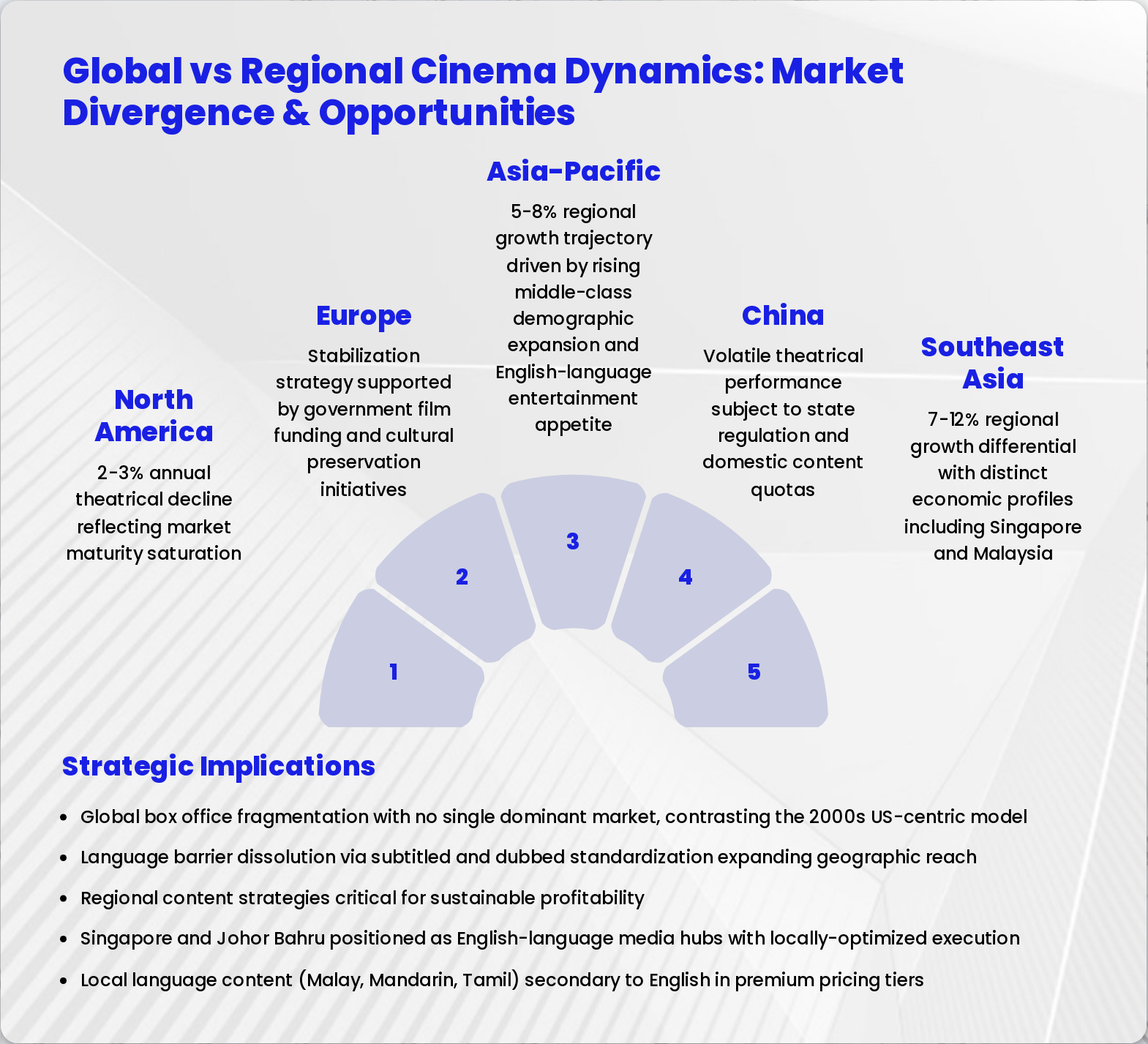

Slide 21: Global vs Regional Cinema Dynamics: Market Divergence & Opportunities

- North America: 2-3% annual theatrical decline reflecting market maturity saturation

- Europe: Stabilization strategy supported by government film funding and cultural preservation initiatives

- Asia-Pacific: 5-8% regional growth trajectory driven by rising middle-class demographic expansion and English-language entertainment appetite

- China: Volatile theatrical performance subject to state regulation and domestic content quotas

- Southeast Asia: 7-12% regional growth differential with distinct economic profiles including Singapore and Malaysia

Global box office fragmentation with no single dominant market, contrasting the 2000s US-centric model

Language barrier dissolution via subtitled and dubbed standardization expanding geographic reach

Regional content strategies critical for sustainable profitability

Singapore and Johor Bahru positioned as English-language media hubs with locally-optimized execution

Local language content (Malay, Mandarin, Tamil) secondary to English in premium pricing tiers

- Global box office fragmentation with no single dominant market, contrasting the 2000s US-centric model

- Language barrier dissolution via subtitled and dubbed standardization expanding geographic reach

- Regional content strategies critical for sustainable profitability

- Singapore and Johor Bahru positioned as English-language media hubs with locally-optimized execution

- Local language content (Malay, Mandarin, Tamil) secondary to English in premium pricing tiers

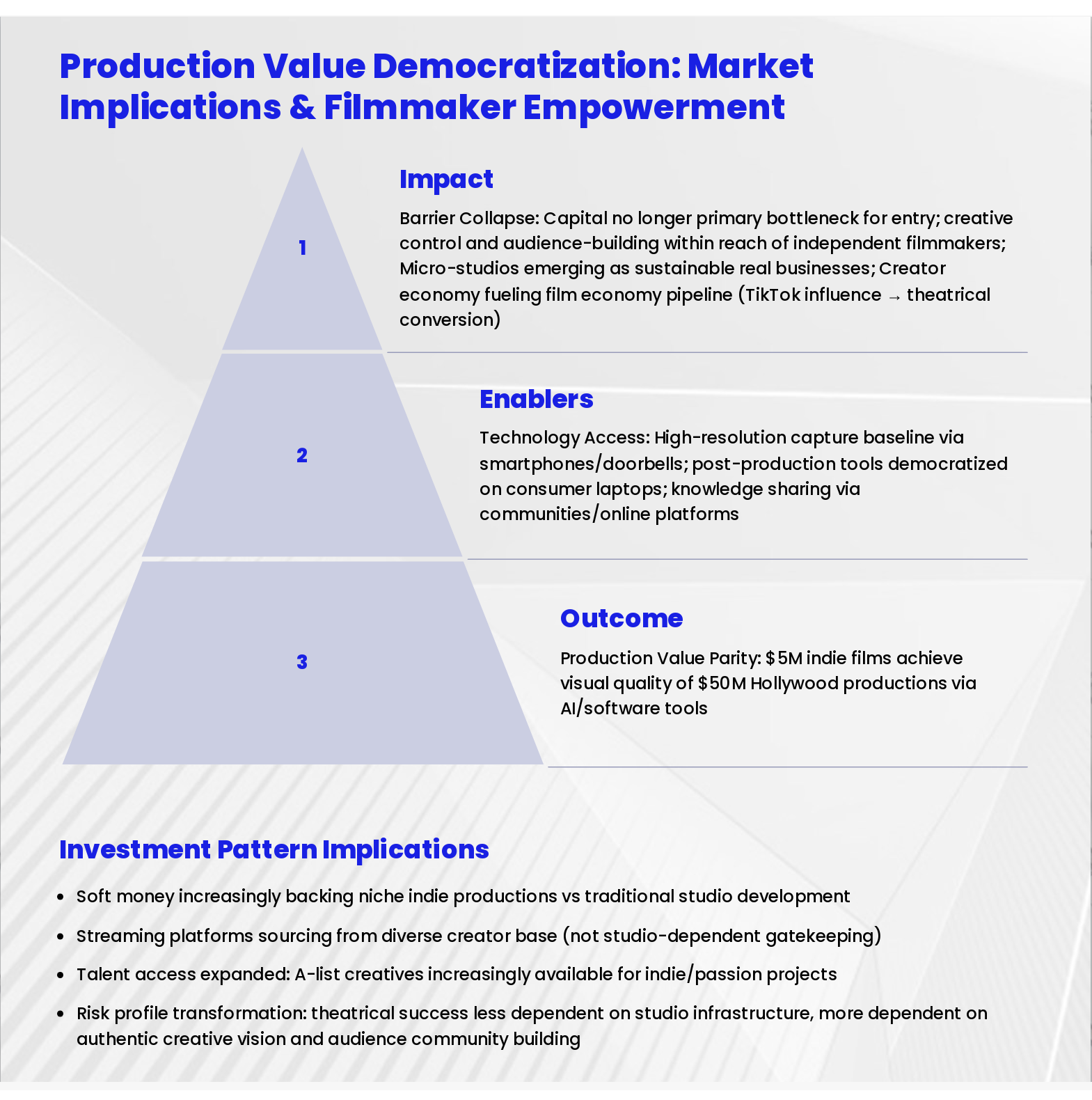

Slide 22: Production Value Democratization: Market Implications & Filmmaker Empowerment

- Impact: Barrier Collapse: Capital no longer primary bottleneck for entry; creative control and audience-building within reach of independent filmmakers; Micro-studios emerging as sustainable real businesses; Creator economy fueling film economy pipeline (TikTok influence → theatrical conversion)

- Enablers: Technology Access: High-resolution capture baseline via smartphones/doorbells; post-production tools democratized on consumer laptops; knowledge sharing via communities/online platforms

- Outcome: Production Value Parity: $5M indie films achieve visual quality of $50M Hollywood productions via AI/software tools

Soft money increasingly backing niche indie productions vs traditional studio development

Streaming platforms sourcing from diverse creator base (not studio-dependent gatekeeping)

Talent access expanded: A-list creatives increasingly available for indie/passion projects

Risk profile transformation: theatrical success less dependent on studio infrastructure, more dependent on authentic creative vision and audience community building

- Soft money increasingly backing niche indie productions vs traditional studio development

- Streaming platforms sourcing from diverse creator base (not studio-dependent gatekeeping)

- Talent access expanded: A-list creatives increasingly available for indie/passion projects

- Risk profile transformation: theatrical success less dependent on studio infrastructure, more dependent on authentic creative vision and audience community building

Slide 23: Economic Outlook2026-2029: Industry Forecasts & Growth Drivers

- $3.5T — Global E&M Market

- $112.7B — OTT Video Segment

- $389.1B — US Digital Advertising

- Gradual — Mixed Reality

- AI-Driven Personalization: AI-powered personalization increasing advertising effectiveness and conversion rates, transforming how content reaches target audiences and monetization strategies evolve

- Asia-Pacific Cinema Recovery: Asia-Pacific cinema recovery outpacing Western market growth with accelerated regional investment. Regional infrastructure expansion including Johor RM140 billion target for 2026signals sustained investment momentum

- Theatrical & Streaming Evolution: Theatrical unit economics improving with per-patron revenue increasing despite lower volume. Streaming consolidation shifting from volume-acquisition to profitability-focused models, redefining financial sustainability

Slide 24: Key Takeaways: Strategic Insights for Cinema Stakeholders

- Market Clarity Achieved: Theatrical stabilized at lower but viable baseline; no recovery expected to 2019 levels; structural demand permanent at reduced volume

- Audience Signals Clear: IP fatigue evident; original stories with distinctive positioning winning market preference; quality-gating replacing volume strategies

- Regional Strategies Critical: Singapore premium positioning (affluence + experience) vs Johor Bahru value arbitrage (currency + cost) represent distinct playbooks requiring tailored execution

- Technology Democratization: AI/tool access enabling production parity across budget tiers; creative execution elevated vs technical bottleneck

- Streaming Coexistence Permanent: Hybrid ecosystem replacing theatrical replacement narrative; complementary monetization (not zero-sum competition)

- Opportunity Positioning 2026: Transitional year establishing sustainable model (not temporary post-pandemic anomaly); soft money flow toward indie/original content; engage cinema as differentiated experience; support original narrative voices; embrace hybrid consumption; leverage regional market characteristics

Slide 25: Cinema's Future: Transformation, Not Decline

The cinema industry evolved fundamentally from 2020-2026 into a sustainable lower-volume, experience-driven, technology-enabled, and globally-connected ecosystem. Success in this landscape requires understanding local market dynamics (Singapore's premium focus vs Johor Bahru's value-driven growth), embracing hybrid consumption models, and participating in the creator economy funnel. The strategic imperative: cinema is not declining—it is transforming into a differentiated premium experience powered by authentic creative voices and enhanced by technology.