How to Lease a Car: A Complete Guide Built with AI Powerpoint

Published on April 29, 2026

Walking into a car dealership can be an overwhelming experience, especially when you are trying to figure out how to lease a car for the first time. Between the technical jargon, the fast-talking sales representatives, and the complex financial calculations, it is easy to feel like you are at a disadvantage. However, leasing offers a flexible way to drive a new vehicle every few years without the long-term commitment of ownership.

This guide is designed to demystify the process, breaking down the financial mechanics and providing a step-by-step roadmap. Whether you are a consumer looking for your next ride or a financial educator using an AI PowerPoint to explain these concepts to a class, this comprehensive walkthrough will ensure you have all the tools necessary to secure the best deal possible.

Understanding the Basics: What Does it Mean to Lease a Car?

At its core, leasing a car is essentially a long-term rental. Instead of paying for the entire value of the vehicle, you are paying for the depreciation that occurs during the period you drive it. Typically, lease terms last between 24 and 48 months. Because you aren't paying for the full equity of the car, your monthly payments are often significantly lower than they would be if you were financing a purchase.

When you learn how to lease a car, you must understand that you are entering a contract with mileage limits and condition requirements. If you exceed the agreed-upon mileage (usually 10,000 to 15,000 miles per year) or return the car with excessive wear and tear, you will face additional fees. It is a perfect arrangement for those who enjoy the latest technology and safety features without the hassle of selling a used car later.

Pro Tip: If you are presenting these options to a client, use an AI Presentation Maker to create a visual side-by-side comparison of leasing versus buying costs over a five-year period.

The Financial Mechanics: Deciphering Leasing Terminology

To truly master how to lease a car, you need to speak the language of the finance office. Most people focus solely on the monthly payment, but that payment is derived from several key variables that are often negotiable.

- Gross Capitalized Cost: This is the "selling price" of the car. Many people don't realize this is negotiable!

- Residual Value: The estimated value of the car at the end of the lease. A higher residual value usually means lower monthly payments.

- Money Factor: This is the interest rate expressed as a decimal. To find the equivalent APR, multiply the money factor by 2400.

- Acquisition Fee: A fee charged by the leasing company for setting up the lease.

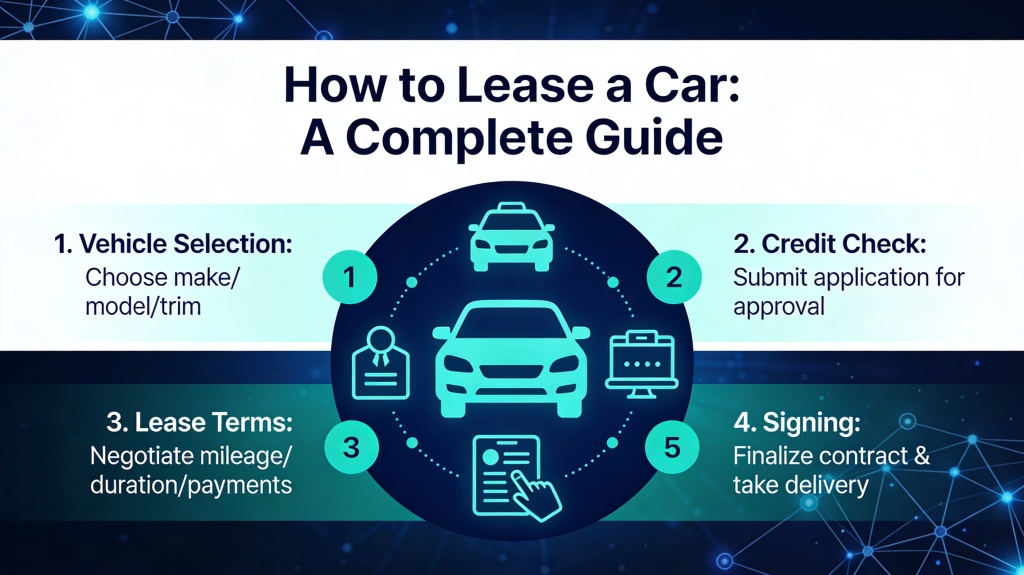

Step-by-Step Guide to the Leasing Process

Knowing how to lease a car involves a logical sequence of actions to ensure you don't overpay. Follow these steps for a smooth experience:

- Check Your Credit Score: Leasing companies generally require higher credit scores than traditional lenders. Ensure your score is above 700 for the best rates.

- Determine Your Budget: Calculate not just the monthly payment, but also insurance, fuel, and the "drive-off" costs (down payment, first month's payment, and fees).

- Research Residual Values: Look for cars that hold their value well. Brands like Honda, Toyota, and Subaru often have high residuals, making them cheaper to lease.

- Get Multiple Quotes: Call the internet sales managers at several dealerships to get their best "out-the-door" lease price for the specific model you want.

- Negotiate the Cap Cost: Focus on the price of the car before talking about monthly payments.

Comparing Leasing vs. Buying: Which is Right for You?

The decision of how to lease a car versus buying one depends entirely on your lifestyle. If you drive 20,000 miles a year, leasing is likely a poor choice due to overage fees. However, if you are a business owner, leasing can offer significant tax advantages as the payment can often be deducted as a business expense.

Buying is an investment in an asset; leasing is a payment for a service. When creating a presentation on this topic, using AI PowerPoint features to generate automated "Pros and Cons" tables can help your audience visualize these trade-offs instantly. Buyers build equity; lessees enjoy lower maintenance risks since the car is usually under warranty for the duration of the lease.

Common Pitfalls and How to Avoid Them

Many first-time lessees fall into traps that cost them thousands. One major mistake is putting too much money down. In a lease, if the car is totaled or stolen two months into the contract, that down payment is often lost forever. It is usually better to do a "zero-down" lease, even if the monthly payment is slightly higher.

Another pitfall is ignoring the "gap insurance." Gap insurance covers the difference between what the car is worth and what you owe if it's totaled. Most modern leases include this, but always verify. Lastly, never lease for longer than the manufacturer's bumper-to-bumper warranty. If the warranty expires at 36 months, don't sign a 48-month lease.

Using AI PowerPoint to Simplify Complex Financial Presentations

Explaining the nuances of how to lease a car—especially the math behind the money factor—can be dry and confusing. This is where AI PowerPoint tools revolutionize the experience. Instead of manually building charts in Excel and pasting them into slides, AI-driven platforms like PopAi allow you to input raw data and generate beautiful, easy-to-understand infographics.

For educators and finance professionals, these tools can generate a full deck on "The Economics of Leasing" in seconds. You can ask the AI to "create a slide explaining the impact of a high residual value on monthly payments," and it will produce a visual representation that is far more effective than a block of text. This ensures your audience remains engaged and leaves with a clear understanding of the financial commitment they are considering.

Frequently Asked Questions

What is the most important factor when learning how to lease a car?

The most important factor is understanding the 'money factor' and the 'residual value,' as these determine your monthly payments and the car's worth at the end of the lease.

Can I negotiate the price of a leased car?

Yes, you can and should negotiate the 'capitalized cost' (the selling price) of the car just as you would if you were buying it. This directly lowers your monthly lease payments.

How can AI PowerPoint help in explaining car leasing?

AI PowerPoint tools like PopAi can automatically generate complex comparison charts, financial breakdowns, and visual aids that make the intricacies of car leasing easy for an audience to understand.

Create your presentation with one click now

Turn complex financial guides into professional slide decks instantly with PopAi's advanced presentation maker.

Try PopAi for Free