Presentation Summary

SpaceX's 2026 IPO is poised to be history's largest public offering, with an $800 billion valuation. This analysis covers SpaceX's business model, IPO timeline, valuation, share pricing, and investment opportunities.

Full Presentation Transcript

Slide 1: SpaceX IPO 2026: The Largest Public Offering in History

Comprehensive Analysis of Valuation, Timeline, and Investment Opportunities

Slide 2: Contents

- Company Background and Business Model: Slides 3–7

- IPO Timeline, Filing Status and Key Dates: Slides 8–10

- Valuation Analysis and Financial Metrics: Slides 11–14

- Share Pricing and Underwriting Structure: Slides 15–16

- Investment Access and Strategic Considerations: Slides 17–20

- Market Implications and Conclusion: Slides 21–23

Slide 3: SpaceX Overview: Revolutionary Aerospace Pioneer Since 2002

- Founded in 2002: Created by Elon Musk with mission to reduce space transportation costs and enable Mars colonization

- Global Operations Hub: Headquarters located in Starbase, Texas with operations spanning launch services, satellite internet, and government contracts

- Massive Valuation: Currently valued at $800 billion in December 2025 private share sale priced at $421 per share

- Advanced Rocket Technology: Cutting-edge reusable rocket technology featuring Falcon 9, Falcon Heavy, and Starship development platforms

- Market Dominance: Over 300 successful launches completed, dominating global commercial launch market with 80%+ market share

- Strategic Ecosystem: Connecting aerospace, telecommunications, artificial intelligence, and national defense sectors

Slide 4: Starlink Global Dominance

- Satellite Constellation: 9,500+ satellites deployed as of early 2024providing global broadband coverage across remote and underserved regions

- Subscriber Base: Exceeding 9 million users globally across residential, commercial, and maritime sectors with rapid expansion

- Revenue Contribution: $7.5-12.8 billion annually representing 50-80% of total company revenue with sustainable growth trajectory

- V3 Expansion: Starlink V3 expansion planned post-IPO to dramatically increase global coverage capacity and internet speeds

- Market Leadership: Business model validated with sustainable profitability achieved since 2023-2024 and first-mover market dominance

Slide 5: SpaceX Launch Services

- Falcon 9: The workhorse rocket with200+ successful launches and fully reusable first stage reducing costs by 30-50%

- Falcon Heavy: Serves as the heavy-lift vehicle for government missions and deep-space commercial missions

- Starship: Next-generation fully reusable super-heavy-lift vehicle under active development for NASA Artemis missions

- Revenue Generation: Launch services generate estimated $3-5 billion annually from commercial, government, and Starlink deployment missions

- Reusability Advantage: Reusability technology provides 5-10 year competitive moat over traditional aerospace launch competitors

- NASA Artemis Contracts: Lunar landing system valued at $2.9 billion include critical development milestones in 2025-2026

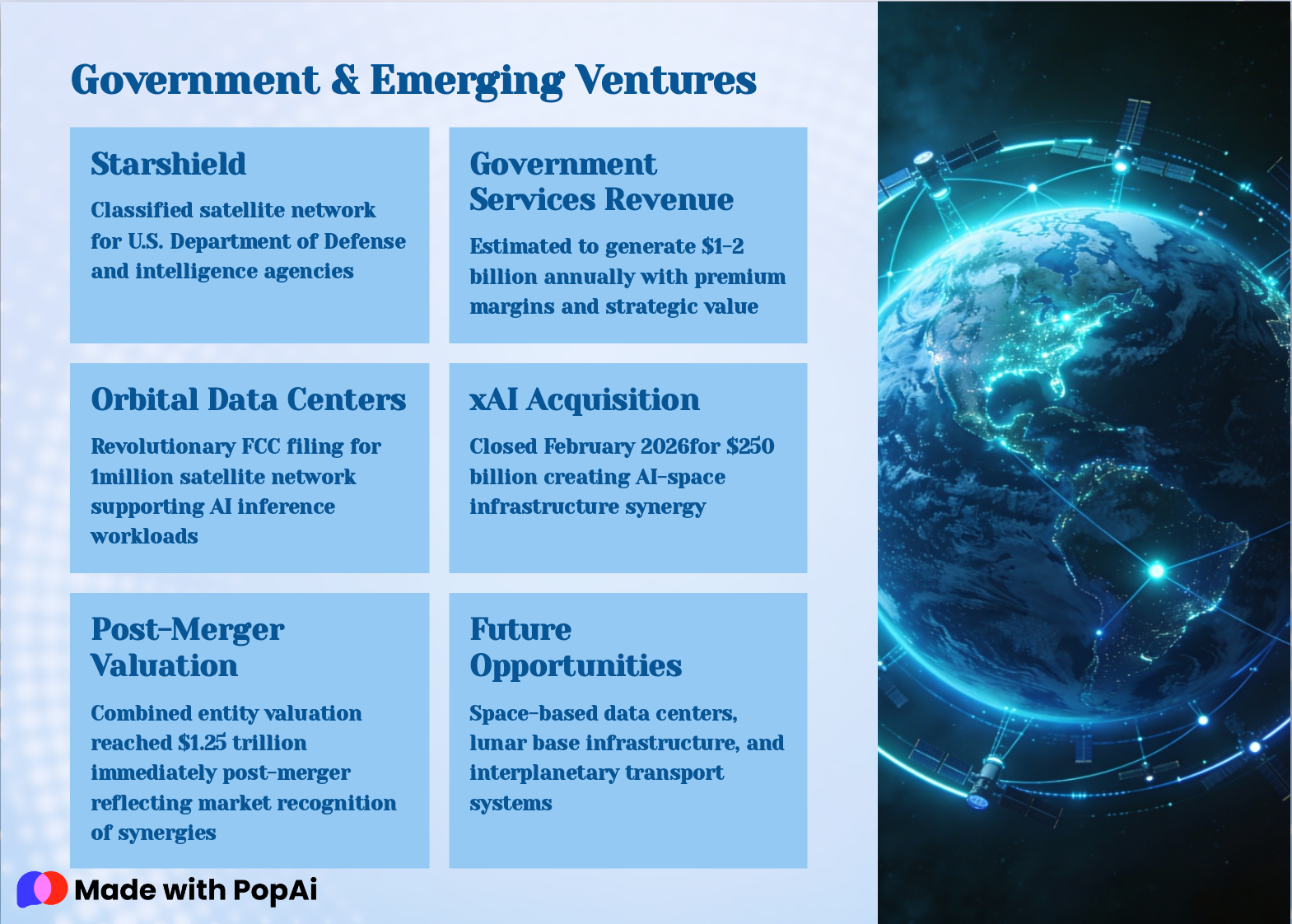

Slide 6: Government & Emerging Ventures

- Starshield: Classified satellite network for U.S. Department of Defense and intelligence agencies

- Government Services Revenue: Estimated to generate $1-2 billion annually with premium margins and strategic value

- Orbital Data Centers: Revolutionary FCC filing for 1million satellite network supporting AI inference workloads

- xAI Acquisition: Closed February 2026for $250 billion creating AI-space infrastructure synergy

- Post-Merger Valuation: Combined entity valuation reached $1.25 trillion immediately post-merger reflecting market recognition of synergies

- Future Opportunities: Space-based data centers, lunar base infrastructure, and interplanetary transport systems

Slide 7: Financial Performance: Explosive Growth with Path to Profitability

- 2023 Revenue: $15–16 billion representing base year before recent acceleration phase

- 2024 Revenue: $13.1 billion confirmed by Sacra showing 51% year-over-year growth from baseline

- 2025 Revenue: $15.5 billion demonstrating 18% growth with increasingly mature business model

- 2025 EBITDA: Approximately $8 billion in operating profit showing strong unit economics

- Margin Expansion: Profit margins continuously improving as Starlink reaches scale and launch reusability reduces marginal costs

- Diversified Growth: Revenue growth trajectory of 18–51% annually with diversified income streams reducing single-product dependency risk

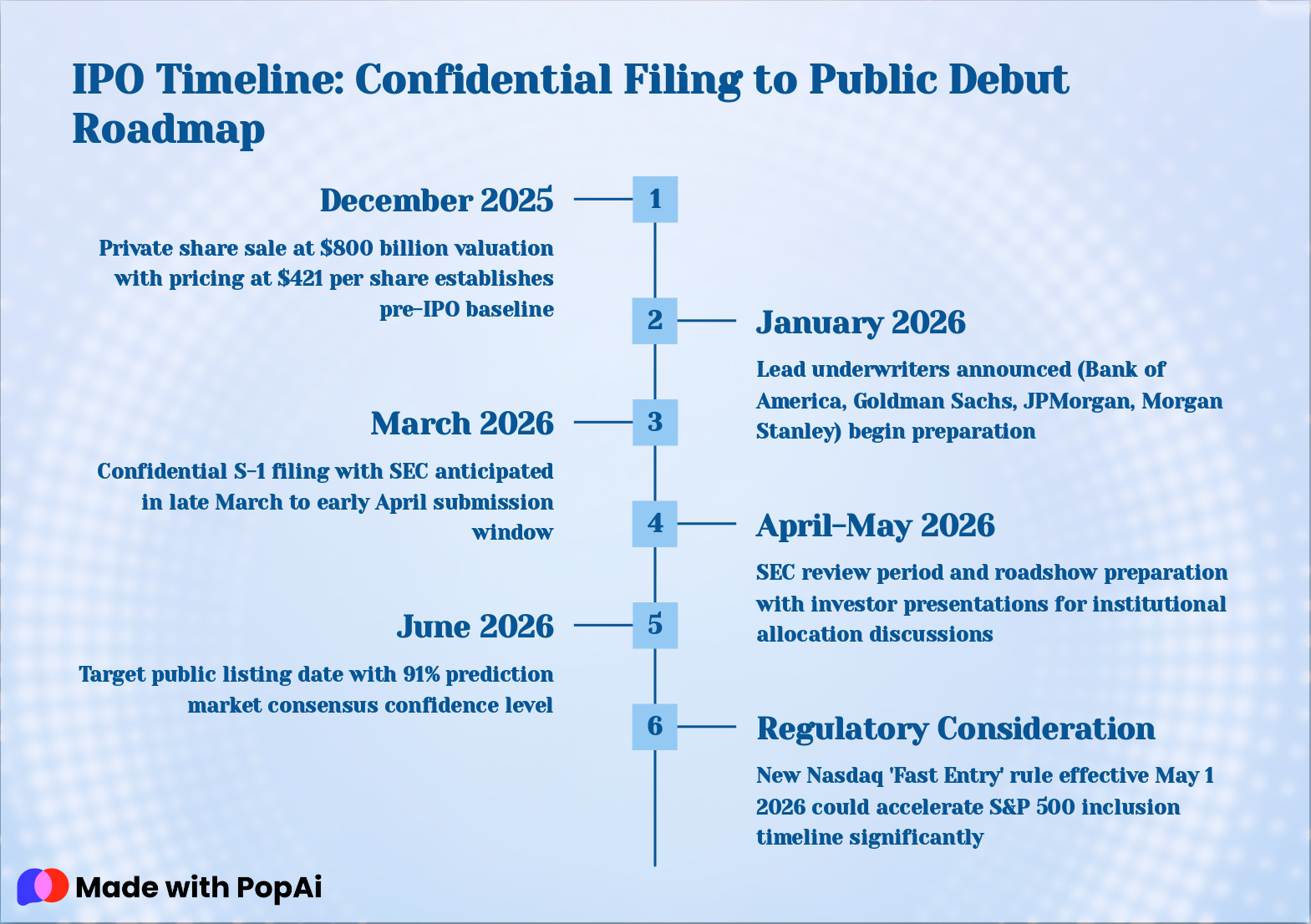

Slide 8: IPO Timeline: Confidential Filing to Public Debut Roadmap

- December 2025: Private share sale at $800 billion valuation with pricing at $421 per share establishes pre-IPO baseline

- January 2026: Lead underwriters announced (Bank of America, Goldman Sachs, JPMorgan, Morgan Stanley) begin preparation

- March 2026: Confidential S-1 filing with SEC anticipated in late March to early April submission window

- April-May 2026: SEC review period and roadshow preparation with investor presentations for institutional allocation discussions

- June 2026: Target public listing date with 91% prediction market consensus confidence level

- Regulatory Consideration: New Nasdaq 'Fast Entry' rule effective May 1 2026 could accelerate S&P 500 inclusion timeline significantly

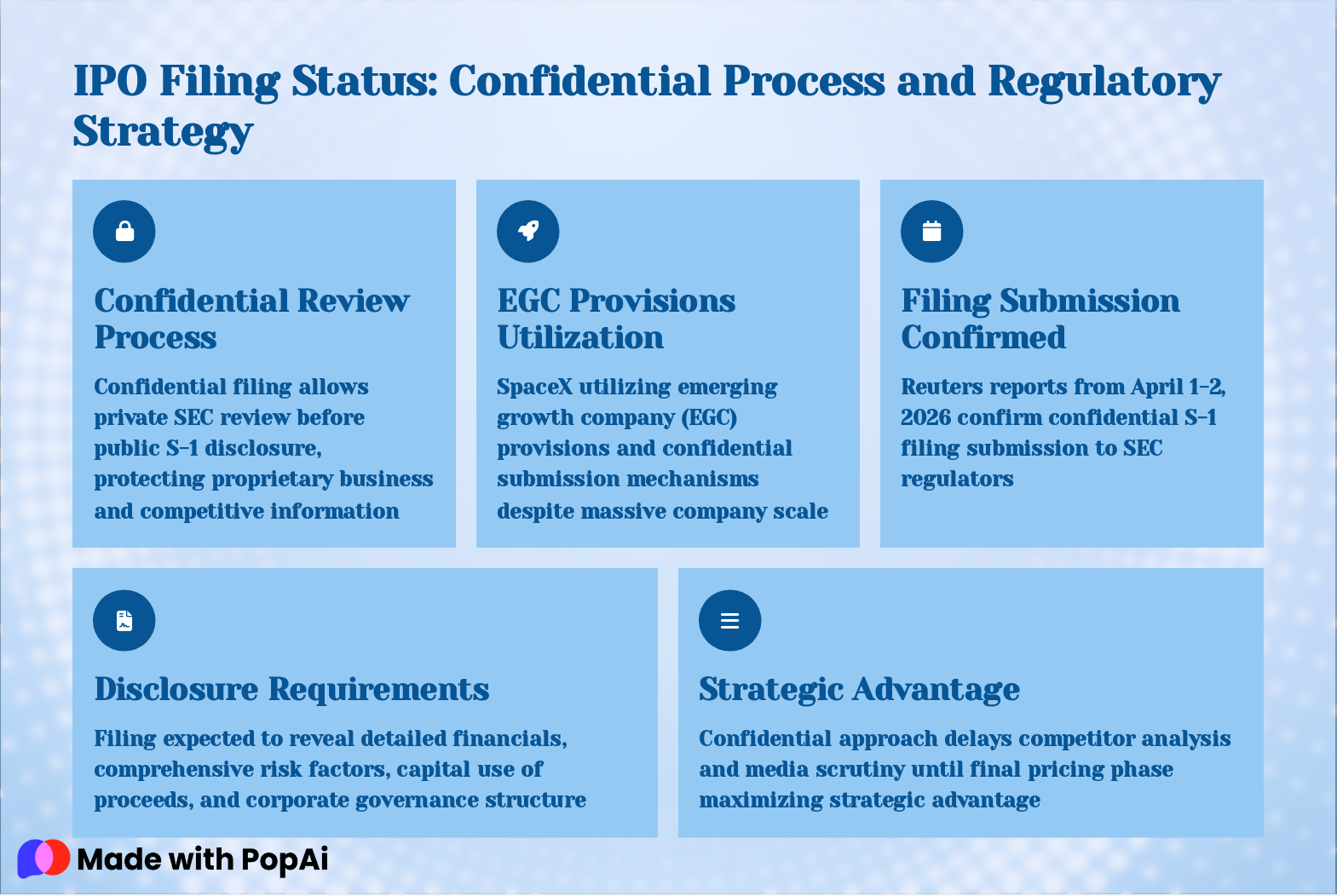

Slide 9: IPO Filing Status: Confidential Process and Regulatory Strategy

- Confidential Review Process: Confidential filing allows private SEC review before public S-1 disclosure, protecting proprietary business and competitive information

- EGC Provisions Utilization: SpaceX utilizing emerging growth company (EGC) provisions and confidential submission mechanisms despite massive company scale

- Filing Submission Confirmed: Reuters reports from April 1-2, 2026 confirm confidential S-1 filing submission to SEC regulators

- Disclosure Requirements: Filing expected to reveal detailed financials, comprehensive risk factors, capital use of proceeds, and corporate governance structure

- Strategic Advantage: Confidential approach delays competitor analysis and media scrutiny until final pricing phase maximizing strategic advantage

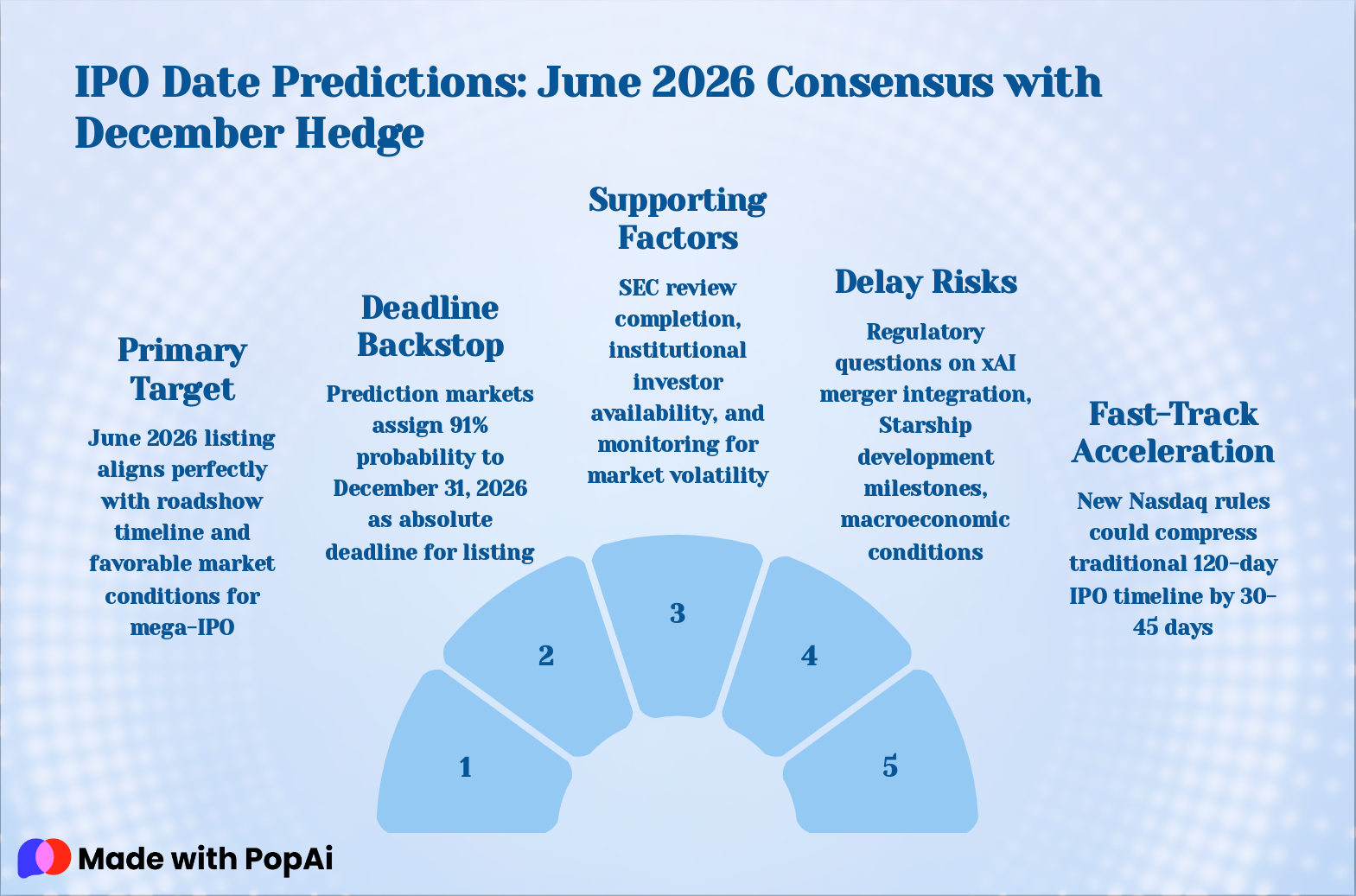

Slide 10: IPO Date Predictions: June 2026 Consensus with December Hedge

- Primary Target: June 2026 listing aligns perfectly with roadshow timeline and favorable market conditions for mega-IPO

- Deadline Backstop: Prediction markets assign 91% probability to December 31, 2026 as absolute deadline for listing

- Supporting Factors: SEC review completion, institutional investor availability, and monitoring for market volatility

- Delay Risks: Regulatory questions on xAI merger integration, Starship development milestones, macroeconomic conditions

- Fast-Track Acceleration: New Nasdaq rules could compress traditional 120-day IPO timeline by 30-45 days

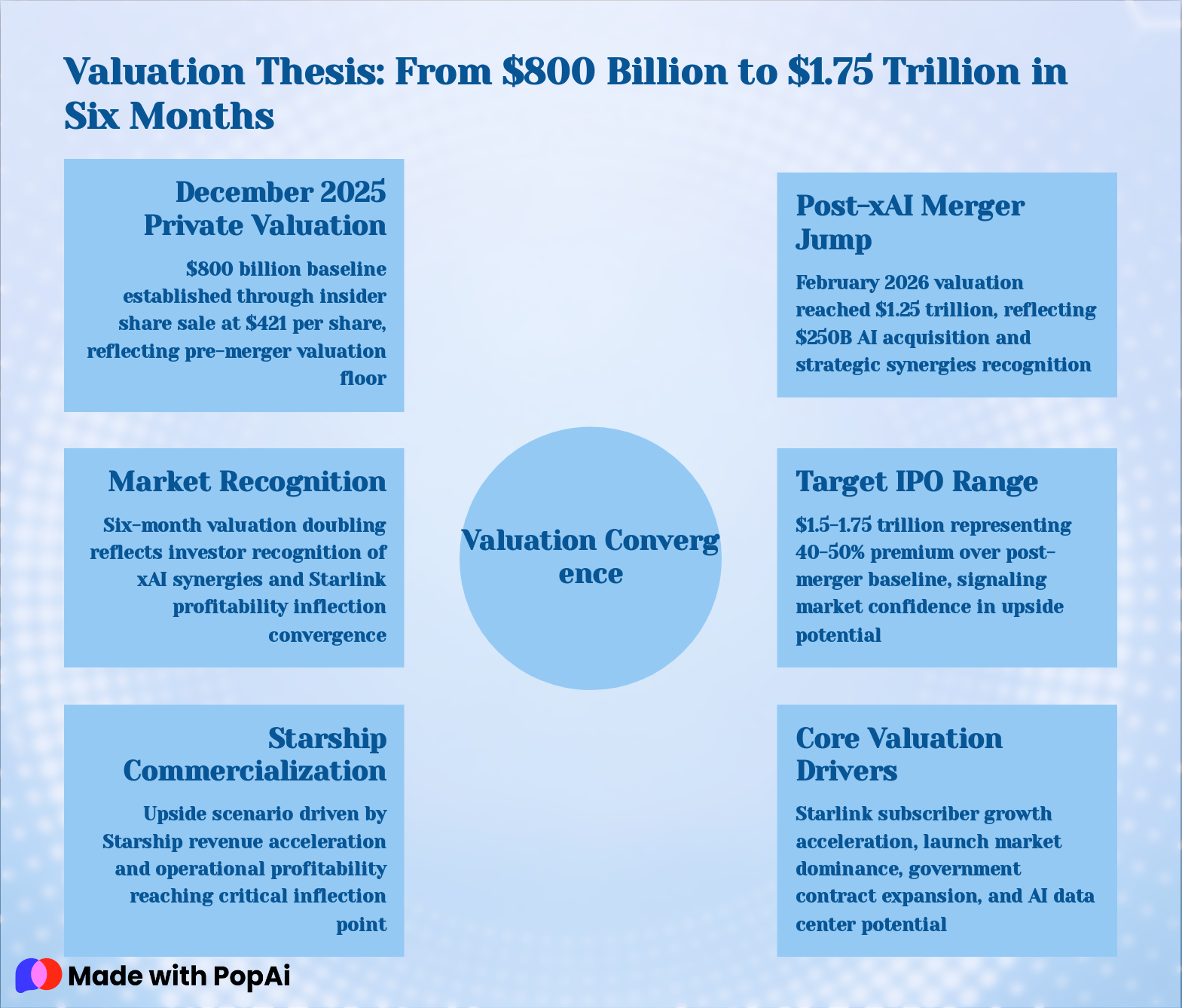

Slide 11: Valuation Thesis: From $800 Billion to $1.75 Trillion in Six Months

- December 2025 Private Valuation: $800 billion baseline established through insider share sale at $421 per share, reflecting pre-merger valuation floor

- Post-xAI Merger Jump: February 2026 valuation reached $1.25 trillion, reflecting $250B AI acquisition and strategic synergies recognition

- Target IPO Range: $1.5-1.75 trillion representing 40-50% premium over post-merger baseline, signaling market confidence in upside potential

- Core Valuation Drivers: Starlink subscriber growth acceleration, launch market dominance, government contract expansion, and AI data center potential

- Starship Commercialization: Upside scenario driven by Starship revenue acceleration and operational profitability reaching critical inflection point

- Market Recognition: Six-month valuation doubling reflects investor recognition of xAI synergies and Starlink profitability inflection convergence

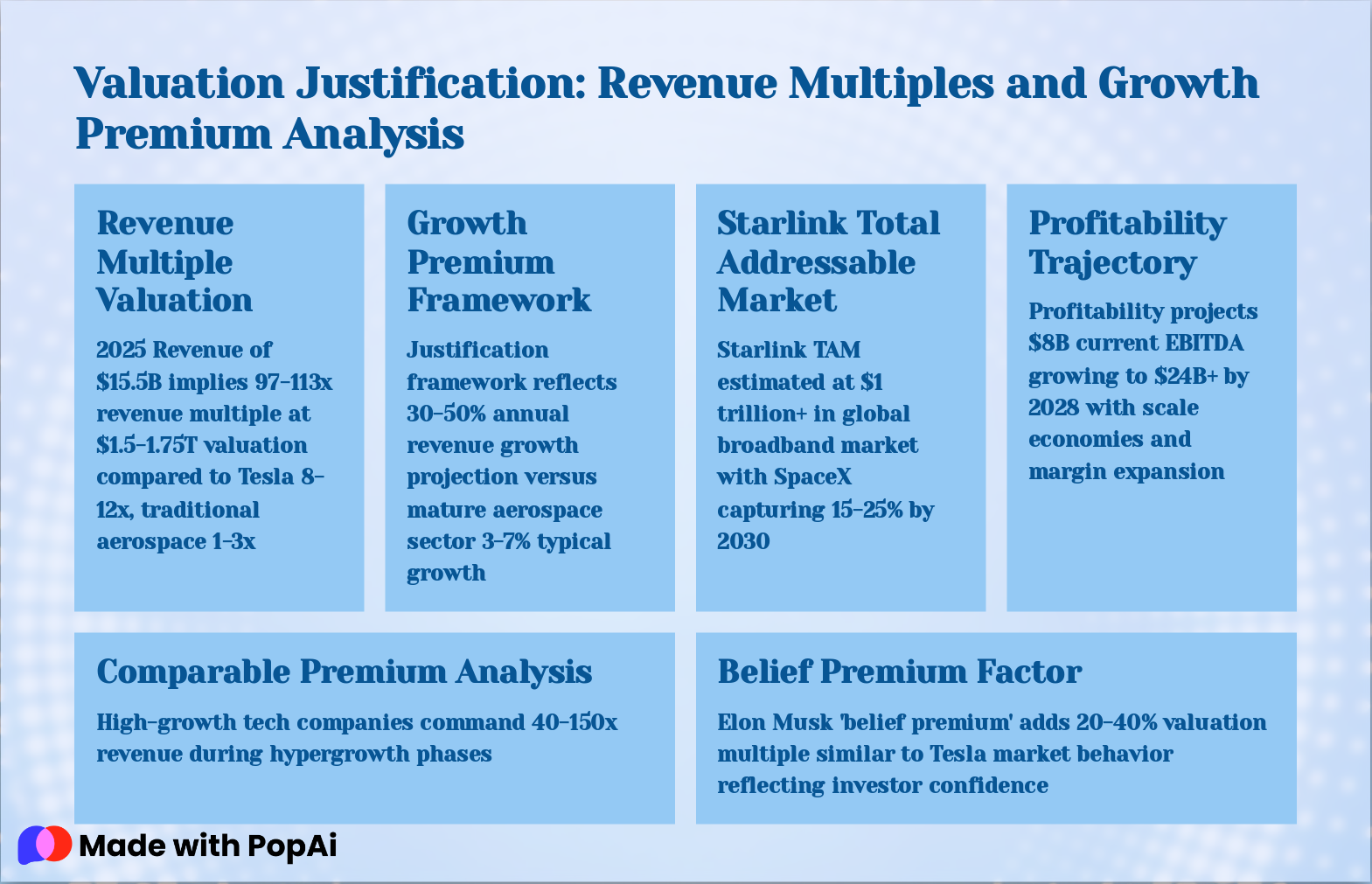

Slide 12: Valuation Justification: Revenue Multiples and Growth Premium Analysis

- Revenue Multiple Valuation: 2025 Revenue of $15.5B implies 97-113x revenue multiple at $1.5-1.75T valuation compared to Tesla 8-12x, traditional aerospace 1-3x

- Growth Premium Framework: Justification framework reflects 30-50% annual revenue growth projection versus mature aerospace sector 3-7% typical growth

- Starlink Total Addressable Market: Starlink TAM estimated at $1 trillion+ in global broadband market with SpaceX capturing 15-25% by 2030

- Profitability Trajectory: Profitability projects $8B current EBITDA growing to $24B+ by 2028 with scale economies and margin expansion

- Comparable Premium Analysis: High-growth tech companies command 40-150x revenue during hypergrowth phases

- Belief Premium Factor: Elon Musk 'belief premium' adds 20-40% valuation multiple similar to Tesla market behavior reflecting investor confidence

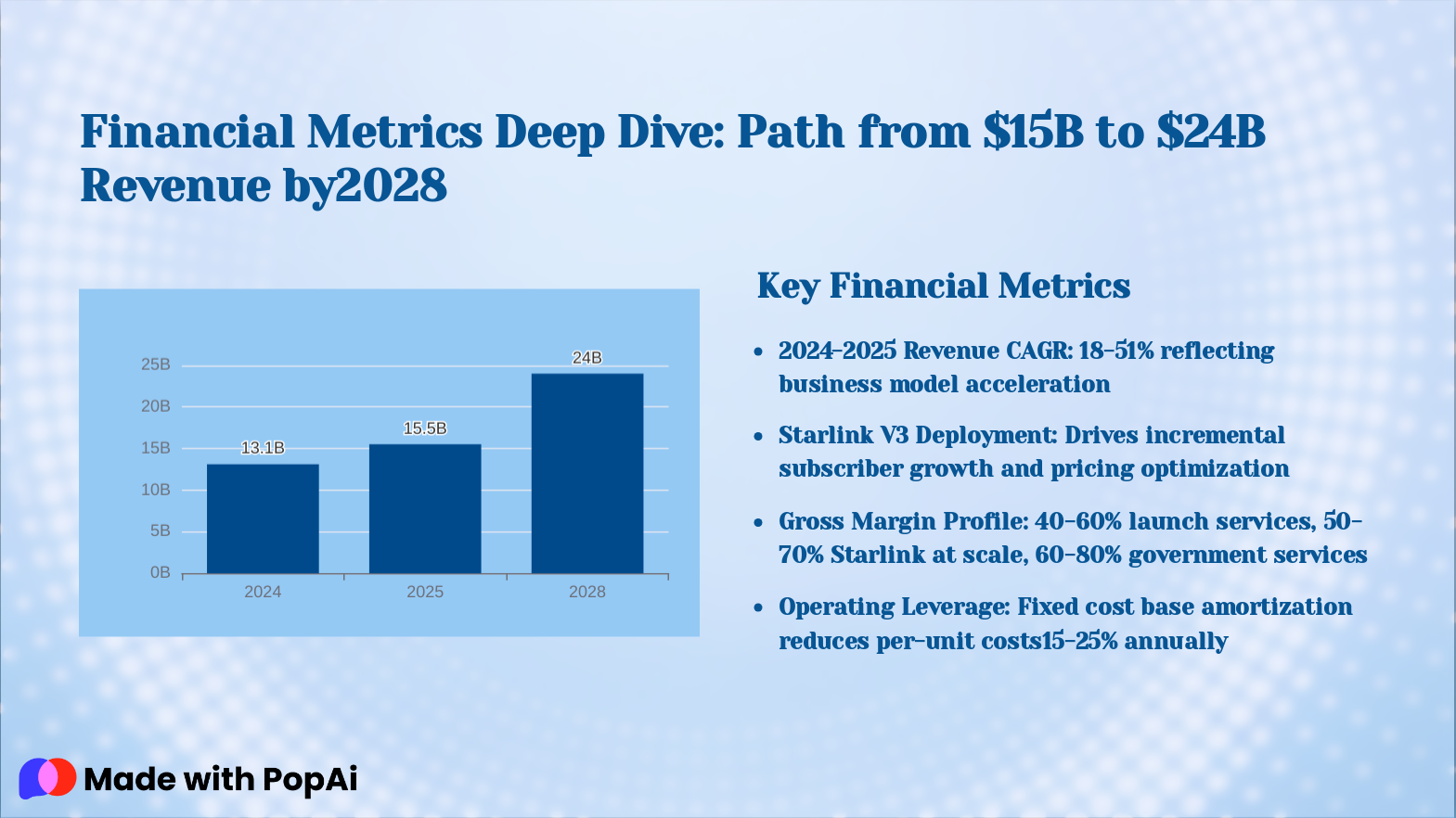

Slide 13: Financial Metrics Deep Dive: Path from $15B to $24B Revenue by2028

2024-2025 Revenue CAGR: 18-51% reflecting business model acceleration

Starlink V3 Deployment: Drives incremental subscriber growth and pricing optimization

Gross Margin Profile: 40-60% launch services, 50-70% Starlink at scale, 60-80% government services

Operating Leverage: Fixed cost base amortization reduces per-unit costs15-25% annually

- 2024-2025 Revenue CAGR: 18-51% reflecting business model acceleration

- Starlink V3 Deployment: Drives incremental subscriber growth and pricing optimization

- Gross Margin Profile: 40-60% launch services, 50-70% Starlink at scale, 60-80% government services

- Operating Leverage: Fixed cost base amortization reduces per-unit costs15-25% annually

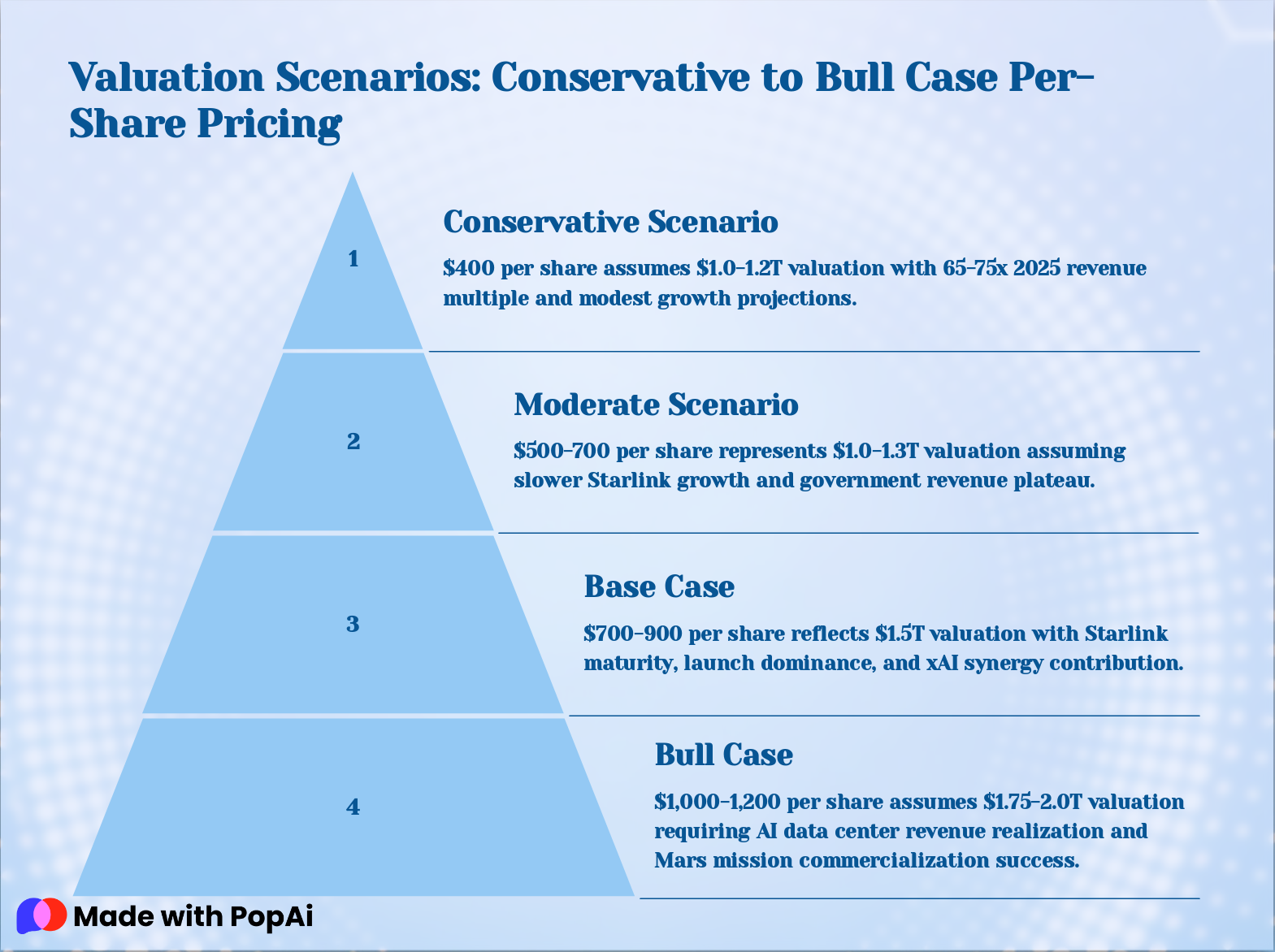

Slide 14: Valuation Scenarios: Conservative to Bull Case Per-Share Pricing

- Conservative Scenario: $400 per share assumes $1.0-1.2T valuation with 65-75x 2025 revenue multiple and modest growth projections.

- Moderate Scenario: $500-700 per share represents $1.0-1.3T valuation assuming slower Starlink growth and government revenue plateau.

- Base Case: $700-900 per share reflects $1.5T valuation with Starlink maturity, launch dominance, and xAI synergy contribution.

- Bull Case: $1,000-1,200 per share assumes $1.75-2.0T valuation requiring AI data center revenue realization and Mars mission commercialization success.

Slide 15: IPO Share Pricing Strategy

- Valuation-Driven Price Range: Anticipated price range of $400-1,200 per share depends on final $1.0-1.75 trillion valuation selection by underwriters

- Midpoint Scenario: Most likely scenario positions $700-900 per share at $1.5trillion midpoint valuation with 1.7-2.0 billion shares outstanding

- Accessibility Pricing: Lower initial price $400-600 maximizes retail investor accessibility and drives enhanced trading volume in secondary markets

- Premium Positioning: Premium pricing $800-1,200 signals strong market confidence and limits equity dilution for existing shareholders

- First-Day Trading Pop: First-day trading expectations include 15-40% typical'pop' for mega-IPOs pushing opening price significantly above initial IPO price

Slide 16: Underwriting Banks: Wall Street's Elite Competing for Historic Mandate

- Lead Underwriters: Bank of America, Goldman Sachs, JPMorgan Chase, and Morgan Stanley occupy senior co-lead roles, positioning themselves at the forefront of this historic mandate

- Hierarchy Redesign: Alphabetical listing of banks represents forgoing traditional 'lead left' position hierarchy to avoid internal competition dynamics and promote equality among co-leads

- Strategic Advantage: Morgan Stanley maintains closest relationship ties to Elon Musk through Tesla banking history providing competitive strategic advantage in execution and deal coordination

- Fee Economics: Underwriting fees estimated at $500M-1.5 billion in total fees (1-2% of $50-75B raise) split among entire syndicate, creating significant revenue opportunity

- Syndicate Structure: Syndicate includes 15-25 additional junior-role banks for regional distribution coverage and institutional investor relationships, expanding market reach

- Banking Competition: Investment banking competition creates largest fee pool in IPO history intensifying bank rivalry for prestige and economics at the highest professional level

Slide 17: How to Buy SpaceX IPO: Institutional Allocation vs. Retail Access Pathways

- Primary Allocation: Reserved for institutional investors and high-net-worth clients of lead underwriting banks

- Retail Investor Access: Limited to brokerage platforms with dedicated IPO access programs (Fidelity, Charles Schwab, Robinhood IPO Access)

- Secondary Market Purchase: Available to all investors on Nasdaq/NYSE after first trading day at market-determined prices

- Pre-IPO Private Markets: Accredited investors can purchase through EquityZen, Forge Global at 5-15% premium to last private valuation

- Alternative Indirect Exposure: ARK Venture Fund (ARKVX) holds 18% SpaceX stake providing indirect liquid access before IPO

Slide 18: Pre-IPO Investment Options

- EquityZen Platform: Enables accredited investors with $200K income or $1M net worth to purchase shares from employees at 5-15% premium

- Forge Global Marketplace: Offers similar secondary market access with typical $100K minimum investment requirements per transaction

- ARK Venture Fund (ARKVX): Holds 17.9% SpaceX allocation providing liquid fund-based exposure with quarterly redemption windows

- Mutual Fund Holdings: Fidelity Contrafund and Baillie Gifford Long Term Global Growth hold undisclosed SpaceX positions

- Liquidity Constraints: Transfer restrictions and limited buyer demand on pre-IPO shares until public listing provides clear exit mechanism

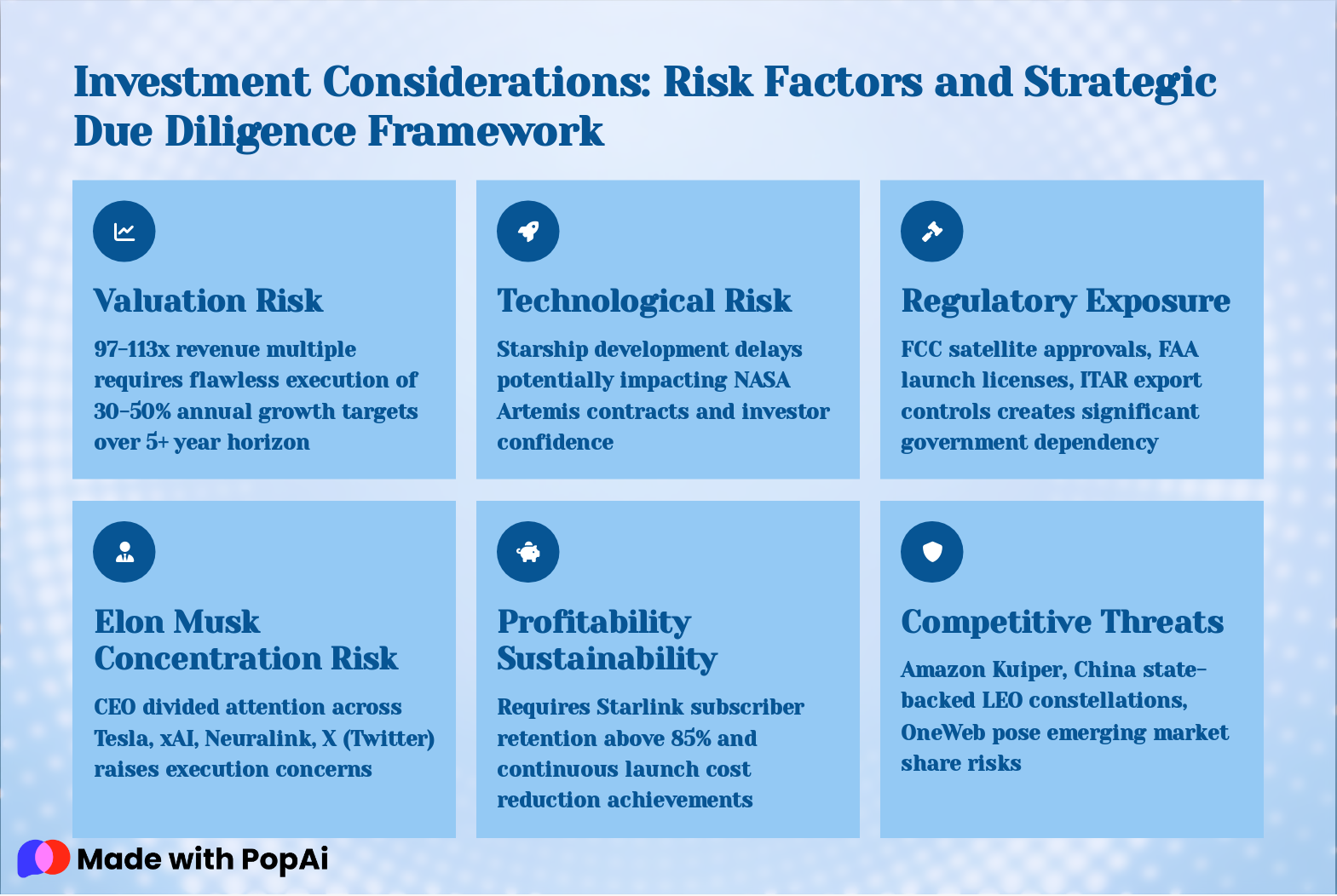

Slide 19: Investment Considerations: Risk Factors and Strategic Due Diligence Framework

- Valuation Risk: 97-113x revenue multiple requires flawless execution of 30-50% annual growth targets over 5+ year horizon

- Technological Risk: Starship development delays potentially impacting NASA Artemis contracts and investor confidence

- Regulatory Exposure: FCC satellite approvals, FAA launch licenses, ITAR export controls creates significant government dependency

- Elon Musk Concentration Risk: CEO divided attention across Tesla, xAI, Neuralink, X (Twitter) raises execution concerns

- Profitability Sustainability: Requires Starlink subscriber retention above 85% and continuous launch cost reduction achievements

- Competitive Threats: Amazon Kuiper, China state-backed LEO constellations, OneWeb pose emerging market share risks

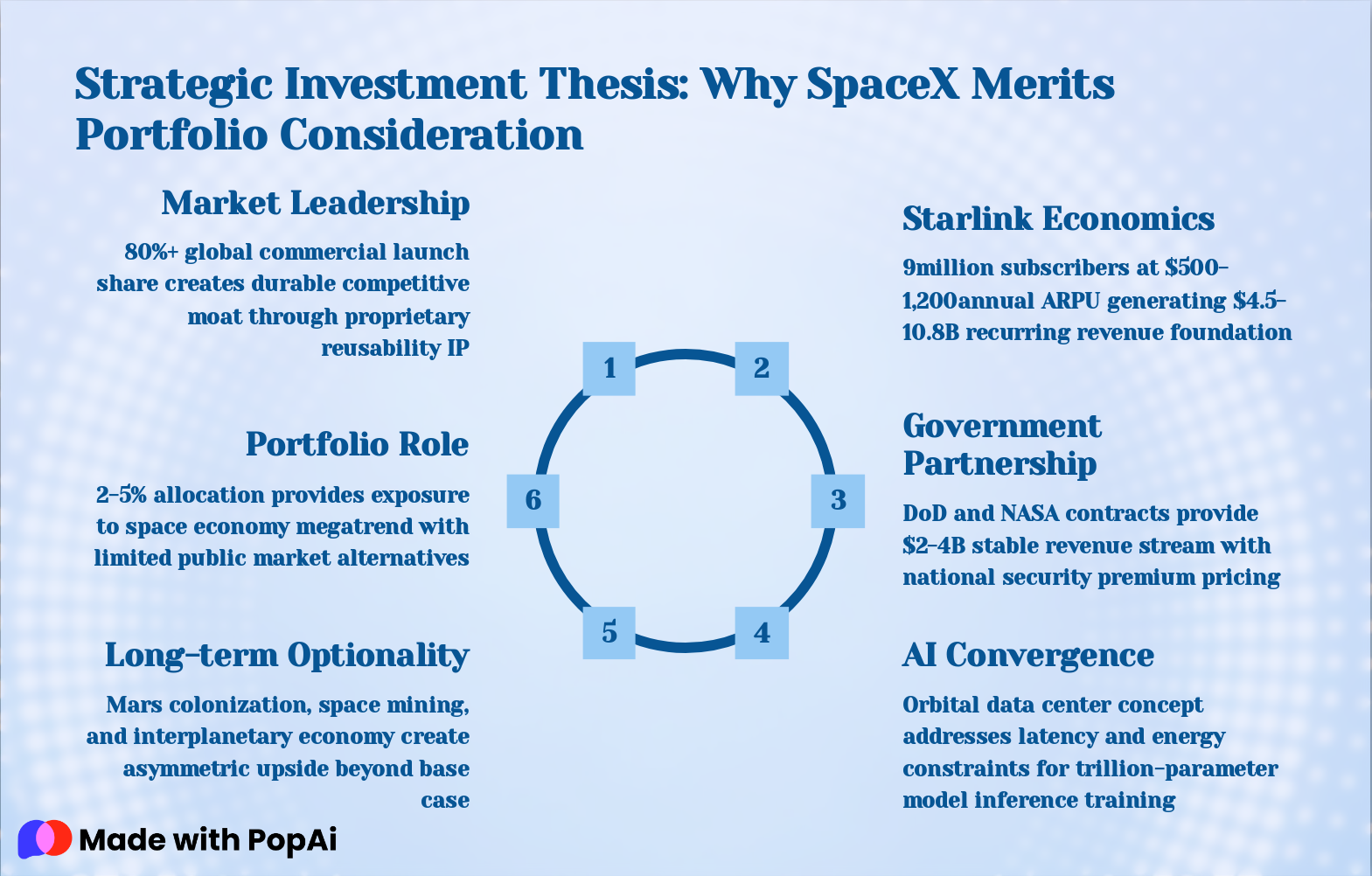

Slide 20: Strategic Investment Thesis: Why SpaceX Merits Portfolio Consideration

- Market Leadership: 80%+ global commercial launch share creates durable competitive moat through proprietary reusability IP

- Starlink Economics: 9million subscribers at $500-1,200annual ARPU generating $4.5-10.8B recurring revenue foundation

- Government Partnership: DoD and NASA contracts provide $2-4B stable revenue stream with national security premium pricing

- AI Convergence: Orbital data center concept addresses latency and energy constraints for trillion-parameter model inference training

- Long-term Optionality: Mars colonization, space mining, and interplanetary economy create asymmetric upside beyond base case

- Portfolio Role: 2-5% allocation provides exposure to space economy megatrend with limited public market alternatives

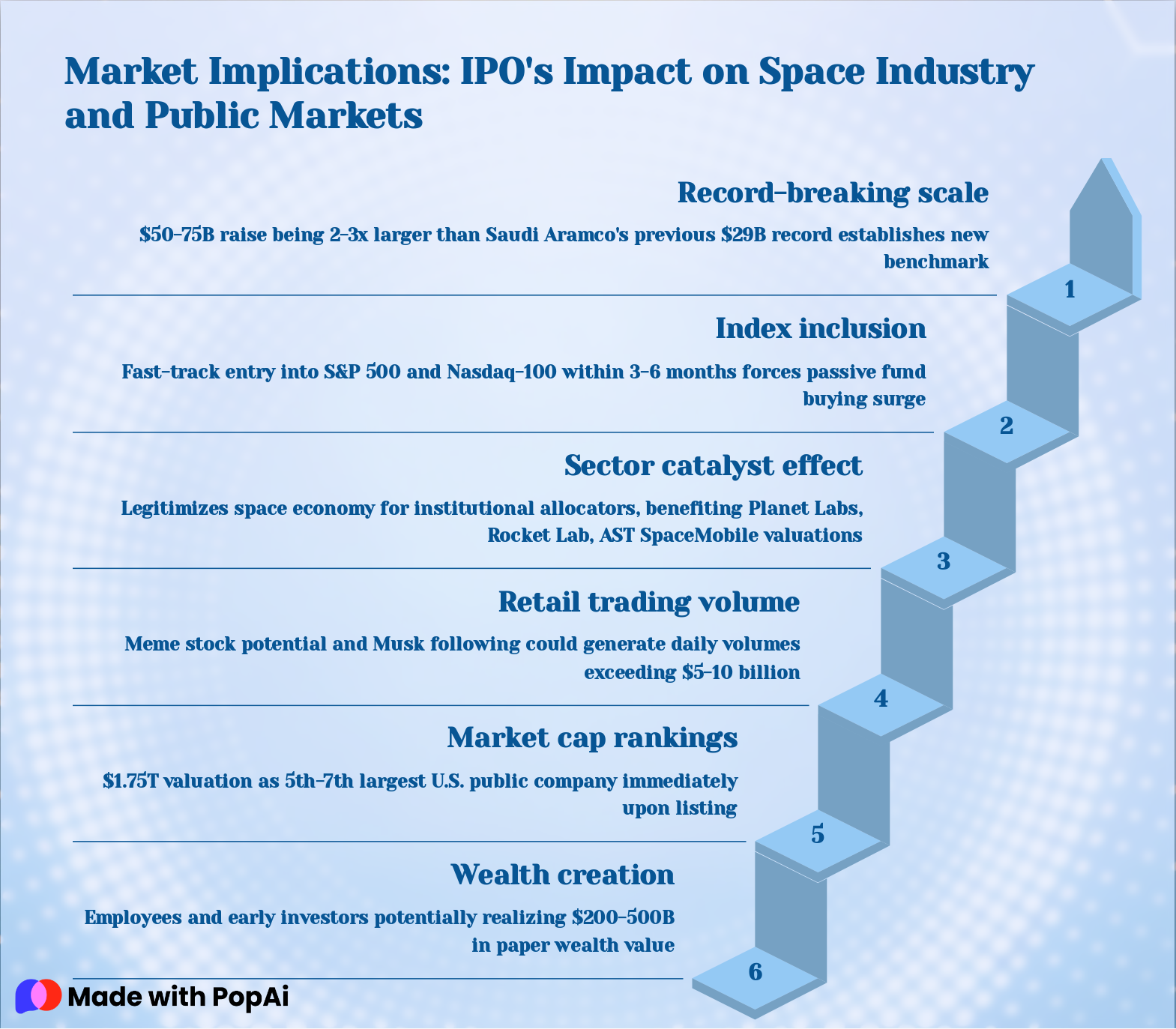

Slide 21: Market Implications: IPO's Impact on Space Industry and Public Markets

- Record-breaking scale: $50-75B raise being 2-3x larger than Saudi Aramco's previous $29B record establishes new benchmark

- Index inclusion: Fast-track entry into S&P 500 and Nasdaq-100 within 3-6 months forces passive fund buying surge

- Sector catalyst effect: Legitimizes space economy for institutional allocators, benefiting Planet Labs, Rocket Lab, AST SpaceMobile valuations

- Retail trading volume: Meme stock potential and Musk following could generate daily volumes exceeding $5-10 billion

- Market cap rankings: $1.75T valuation as 5th-7th largest U.S. public company immediately upon listing

- Wealth creation: Employees and early investors potentially realizing $200-500B in paper wealth value

Slide 22: 2026 IPO Pipeline

- SpaceX Anchor IPO: SpaceX acts as anchor IPO with June 2026 debut setting valuation benchmarks and investor appetite for space technology sector

- AI Mega-IPO Cycle: Follow-on IPOs including OpenAI, Anthropic AI companies also targeting2026 listings creating technology mega-IPO cycle

- Competitive Pressure: Competitive dynamics where Amazon Kuiper remains private but SpaceX IPO may pressure Jeff Bezos to accelerate public listing timeline

- Sector Winners: Sector winners including public space stocks (Rocket Lab, Planet Labs) benefit from rising sector multiples and institutional interest surge

- Institutional Positioning: Institutional positioning showing hedge funds, sovereign wealth funds, pension funds increasing space economy allocations from under 1% to 3-5% of portfolios

Slide 23: Conclusion: Generational Investment Opportunity with Calculated Risks

Conclusion: Generational Investment Opportunity with Calculated Risks Investment thesis offers exposure to space economy leader with validated $15.5B revenue base and proven business model; Valuation reality demands 30%+ annual growth and flawless execution over 5-7 year horizon at $1.5-1.75T pricin...