Presentation Summary

Mastering the 50/30/20 Rule, Emergency Funds, Expense Tracking & Debt Elimination Strategies 78% of Americans report living paycheck-to-paycheck, highlighting widespread financial fragility across demographics. Financial insecurity ranks as the top driver of anxiety, affecting daily decision-making and long-term planning. Four core frameworks provide a clear roadmap for improving financial resilience and habits. With the right budgeting practices, anyone can regain control and build sustainable financial health. Financial stress is a leading cause of anxiety in modern life, producing chronic w

Full Presentation Transcript

Slide 1: Personal Finance Basics: Budgeting 101

Mastering the 50/30/20 Rule, Emergency Funds, Expense Tracking & Debt Elimination Strategies

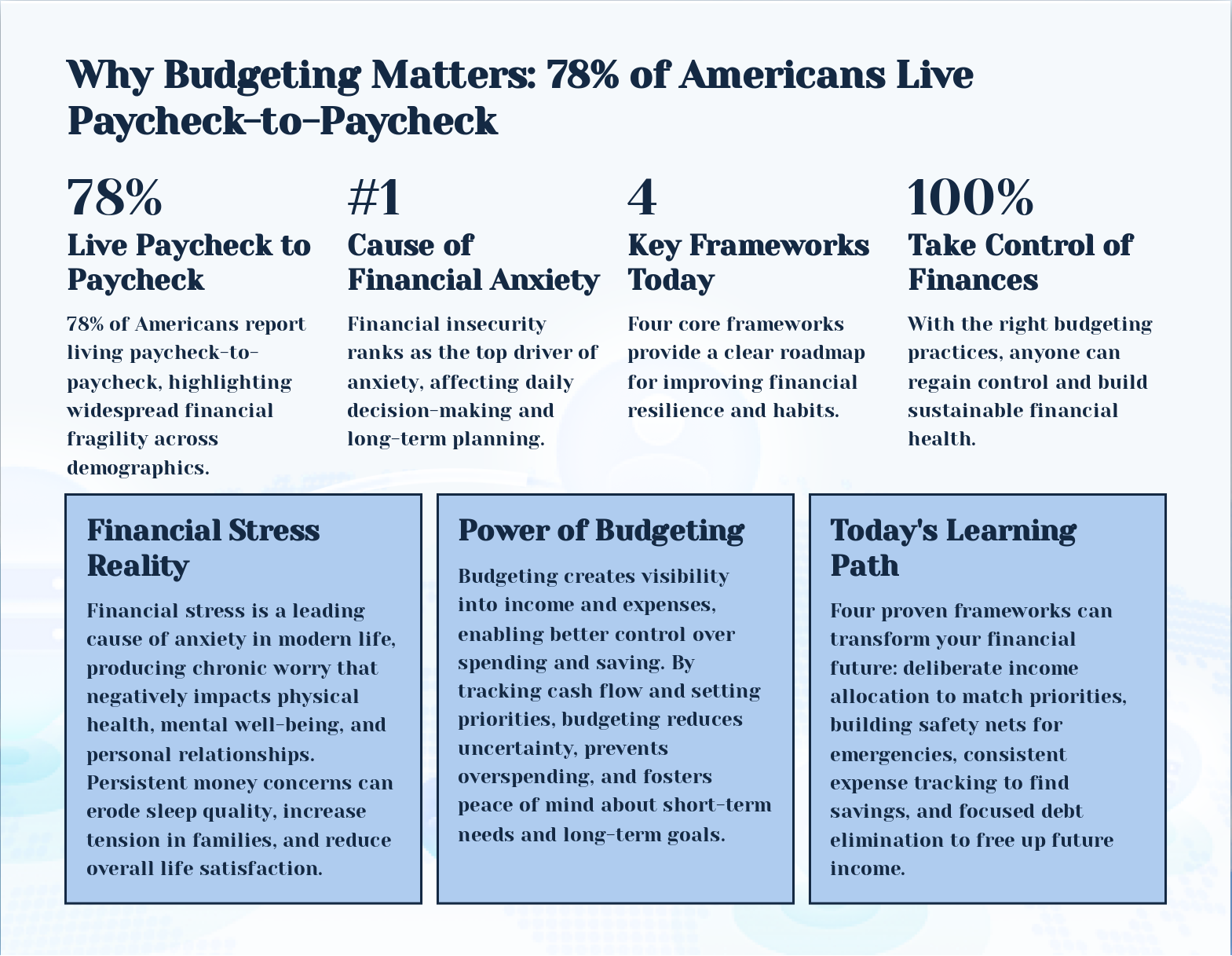

Slide 2: Why Budgeting Matters: 78% of Americans Live Paycheck-to-Paycheck

- 78% — Live Paycheck to Paycheck

- #1 — Cause of Financial Anxiety

- 4 — Key Frameworks Today

- 100% — Take Control of Finances

- Financial Stress Reality: Financial stress is a leading cause of anxiety in modern life, producing chronic worry that negatively impacts physical health, mental well-being, and personal relationships. Persistent money concerns can erode sleep quality, increase tension in families, and reduce overall life satisfaction.

- Power of Budgeting: Budgeting creates visibility into income and expenses, enabling better control over spending and saving. By tracking cash flow and setting priorities, budgeting reduces uncertainty, prevents overspending, and fosters peace of mind about short-term needs and long-term goals.

- Today's Learning Path: Four proven frameworks can transform your financial future: deliberate income allocation to match priorities, building safety nets for emergencies, consistent expense tracking to find savings, and focused debt elimination to free up future income.

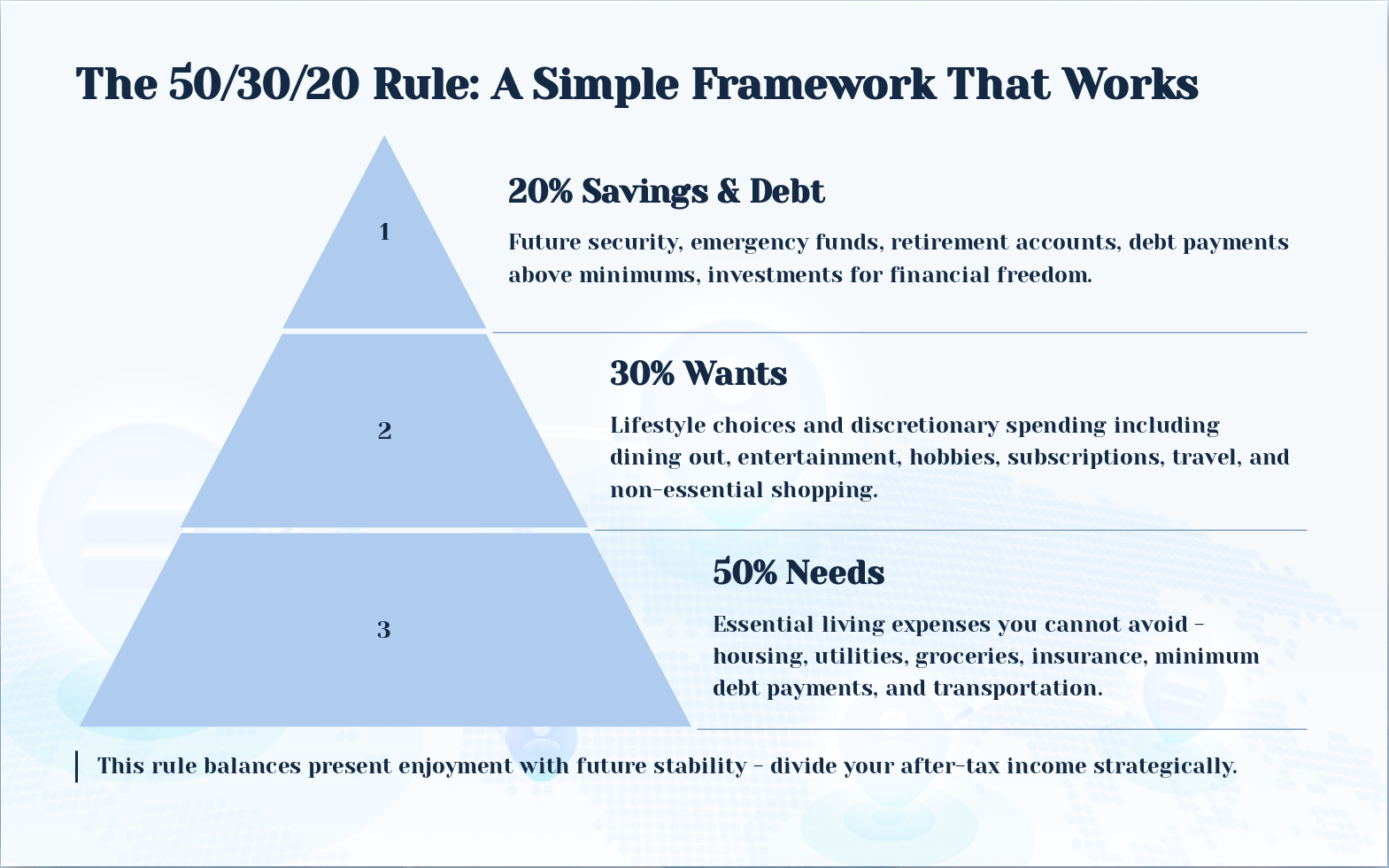

Slide 3: The 50/30/20 Rule: A Simple Framework That Works

- 20% Savings & Debt: Future security, emergency funds, retirement accounts, debt payments above minimums, investments for financial freedom.

- 30% Wants: Lifestyle choices and discretionary spending including dining out, entertainment, hobbies, subscriptions, travel, and non-essential shopping.

- 50% Needs: Essential living expenses you cannot avoid - housing, utilities, groceries, insurance, minimum debt payments, and transportation.

This rule balances present enjoyment with future stability - divide your after-tax income strategically.

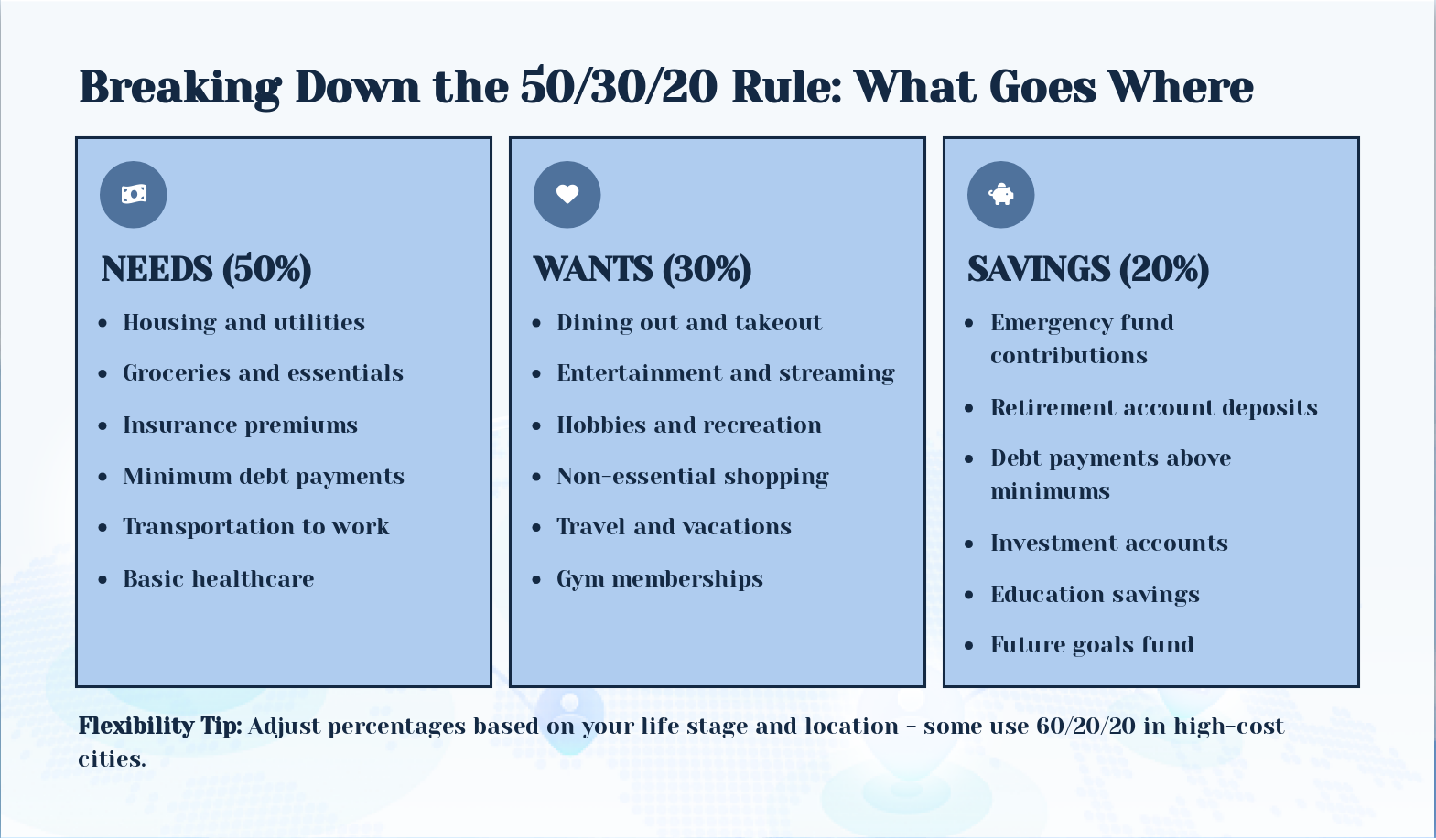

Slide 4: Breaking Down the 50/30/20 Rule: What Goes Where

- NEEDS (50%): Housing and utilities

- WANTS (30%): Dining out and takeout

- SAVINGS (20%): Emergency fund contributions

Flexibility Tip: Adjust percentages based on your life stage and location - some use 60/20/20 in high-cost cities.

Slide 5: Emergency Funds: Your Financial Safety Net

- Purpose of Emergency Funds: Cover unexpected expenses without derailing your budget or going into debt - your financial shock absorber.

- Target Amount: Save 3-6 months of essential living expenses in an accessible, high-yield savings account.

- When to Use: Job loss, medical emergencies, major home or car repairs, urgent family situations - true emergencies only.

- The Psychological Benefit: Reduces financial anxiety dramatically and enables better decision-making without panic.

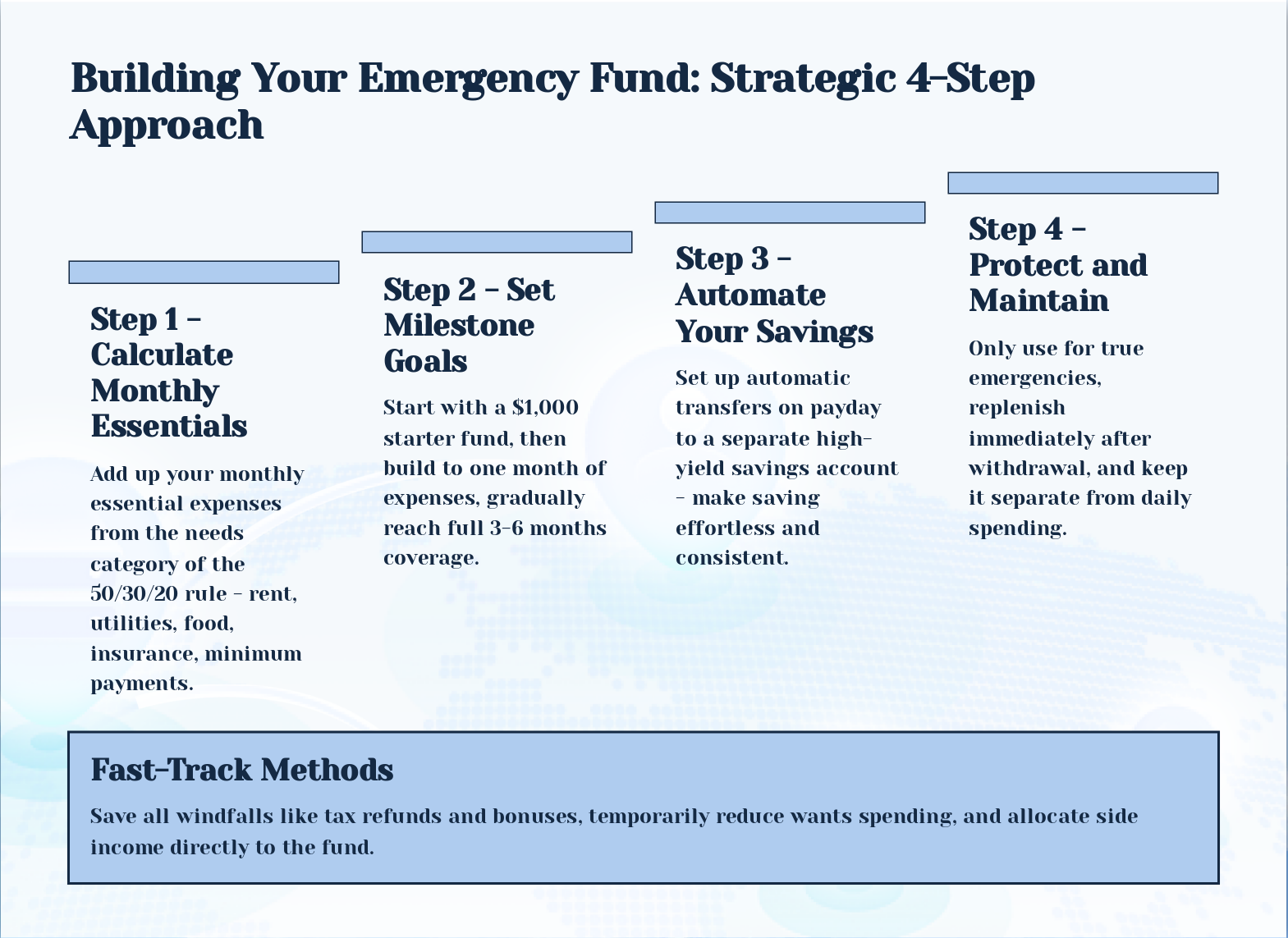

Slide 6: Building Your Emergency Fund: Strategic 4-Step Approach

- Step 1 - Calculate Monthly Essentials: Add up your monthly essential expenses from the needs category of the 50/30/20 rule - rent, utilities, food, insurance, minimum payments.

- Step 2 - Set Milestone Goals: Start with a $1,000 starter fund, then build to one month of expenses, gradually reach full 3-6 months coverage.

- Step 3 - Automate Your Savings: Set up automatic transfers on payday to a separate high-yield savings account - make saving effortless and consistent.

- Step 4 - Protect and Maintain: Only use for true emergencies, replenish immediately after withdrawal, and keep it separate from daily spending.

- Fast-Track Methods: Save all windfalls like tax refunds and bonuses, temporarily reduce wants spending, and allocate side income directly to the fund.

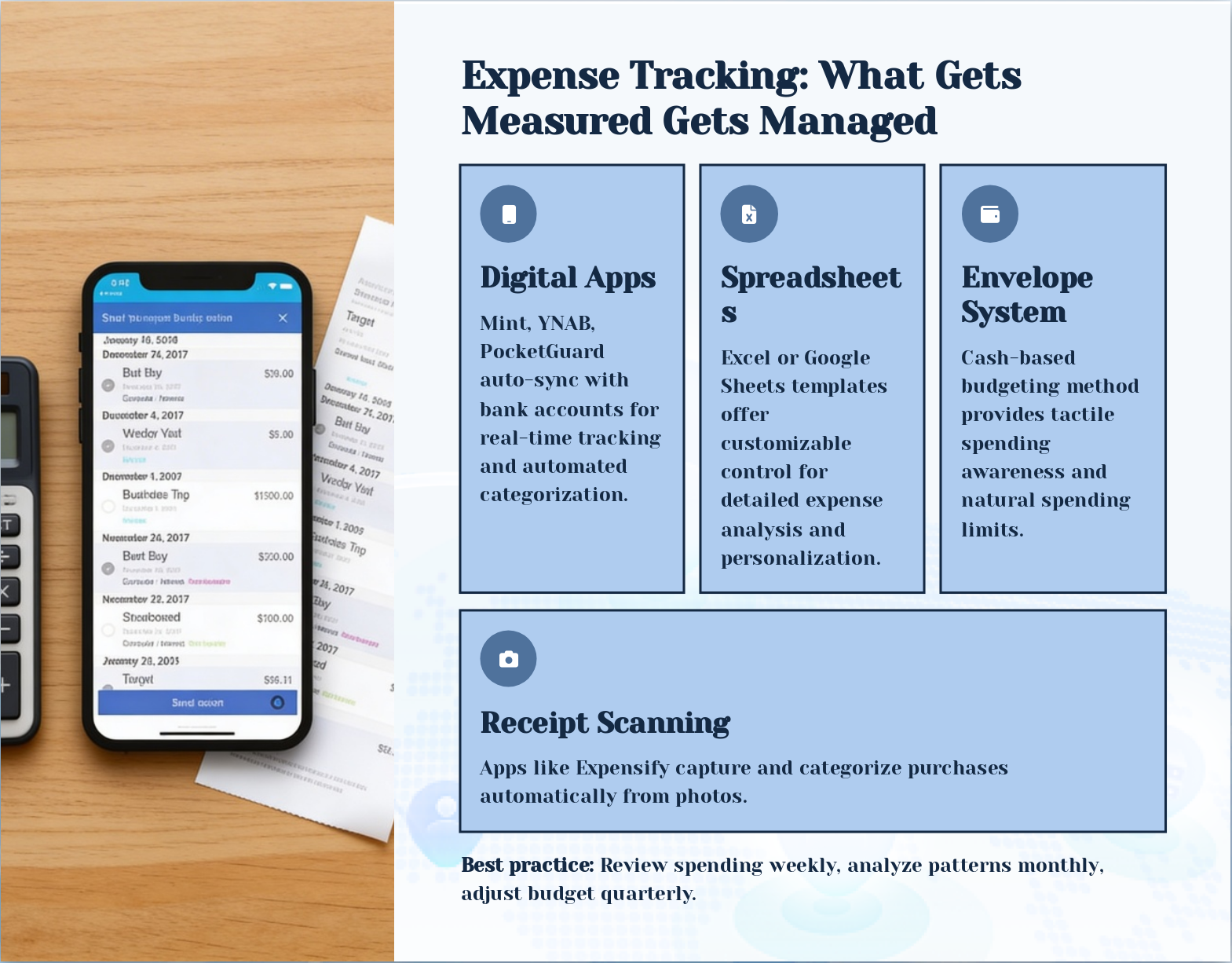

Slide 7: Expense Tracking: What Gets Measured Gets Managed

- Digital Apps: Mint, YNAB, PocketGuard auto-sync with bank accounts for real-time tracking and automated categorization.

- Spreadsheets: Excel or Google Sheets templates offer customizable control for detailed expense analysis and personalization.

- Envelope System: Cash-based budgeting method provides tactile spending awareness and natural spending limits.

- Receipt Scanning: Apps like Expensify capture and categorize purchases automatically from photos.

Best practice: Review spending weekly, analyze patterns monthly, adjust budget quarterly.

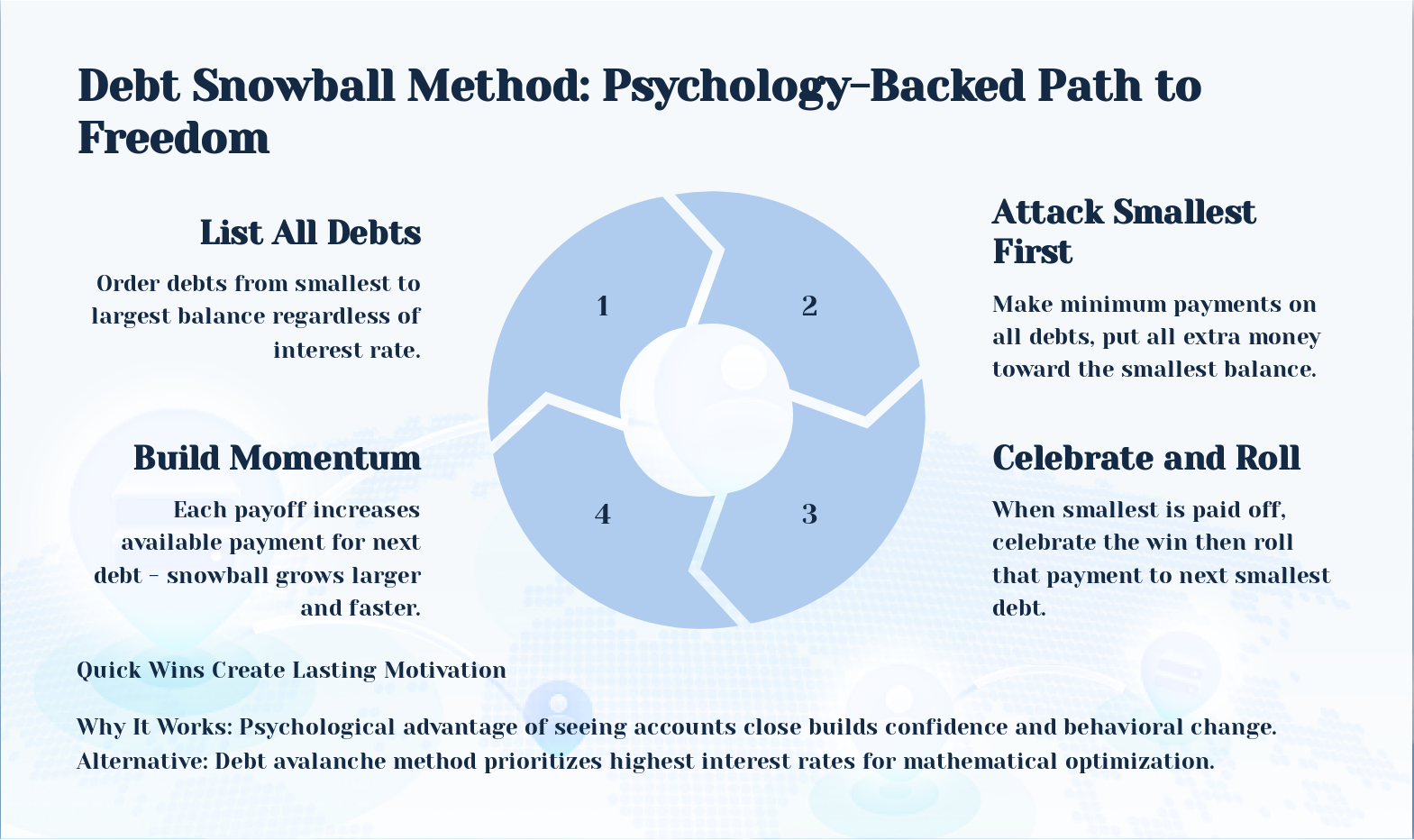

Slide 8: Debt Snowball Method: Psychology-Backed Path to Freedom

- List All Debts: Order debts from smallest to largest balance regardless of interest rate.

- Attack Smallest First: Make minimum payments on all debts, put all extra money toward the smallest balance.

- Celebrate and Roll: When smallest is paid off, celebrate the win then roll that payment to next smallest debt.

- Build Momentum: Each payoff increases available payment for next debt - snowball grows larger and faster.

Quick Wins Create Lasting Motivation

Why It Works: Psychological advantage of seeing accounts close builds confidence and behavioral change. Alternative: Debt avalanche method prioritizes highest interest rates for mathematical optimization.

Slide 9: Debt Snowball in Action: Real-World Example

- Summary: Strategy: Pay minimums on all debts, apply extra $200/month to smallest debt first. Results: Debt-free in 36 months versus 60+ months with minimum-only payments - save years of stress and interest.

- Debt Name: Credit Card A, Balance: $500, Minimum Payment: $25, Order: 1st Priority, Payoff Timeline: Month 1-3

- Debt Name: Credit Card B, Balance: $2,000, Minimum Payment: $50, Order: 2nd Priority, Payoff Timeline: Month 4-12

- Debt Name: Car Loan, Balance: $8,000, Minimum Payment: $250, Order: 3rd Priority, Payoff Timeline: Month 13-24

- Debt Name: Student Loan, Balance: $15,000, Minimum Payment: $150, Order: Final Priority, Payoff Timeline: Month 25-36

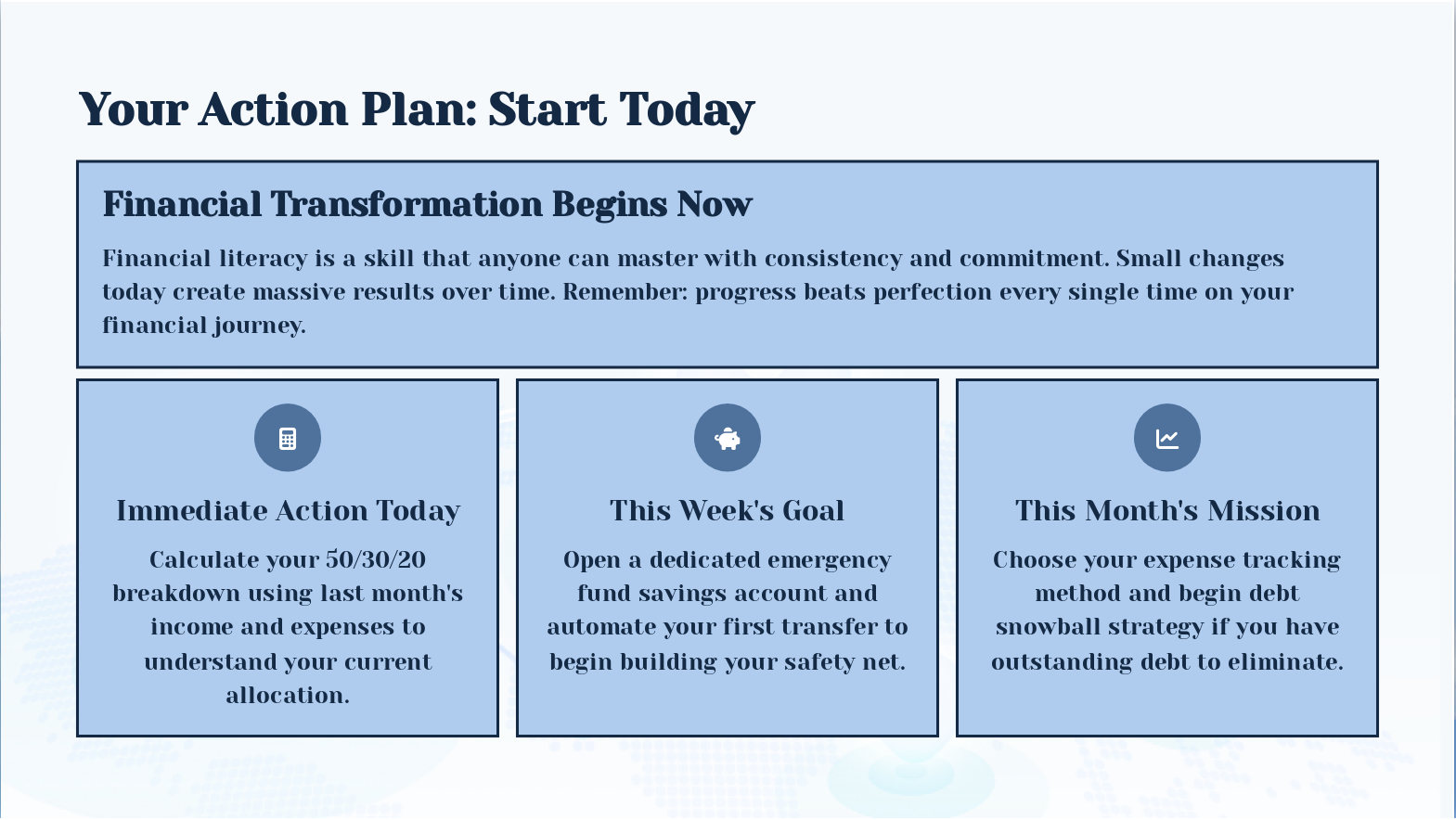

Slide 10: Your Action Plan: Start Today

- Financial Transformation Begins Now: Financial literacy is a skill that anyone can master with consistency and commitment. Small changes today create massive results over time. Remember: progress beats perfection every single time on your financial journey.

- Immediate Action Today: Calculate your 50/30/20 breakdown using last month's income and expenses to understand your current allocation.

- This Week's Goal: Open a dedicated emergency fund savings account and automate your first transfer to begin building your safety net.

- This Month's Mission: Choose your expense tracking method and begin debt snowball strategy if you have outstanding debt to eliminate.